December Mid-Month Market Update

Silent Dissents at the December FOMC

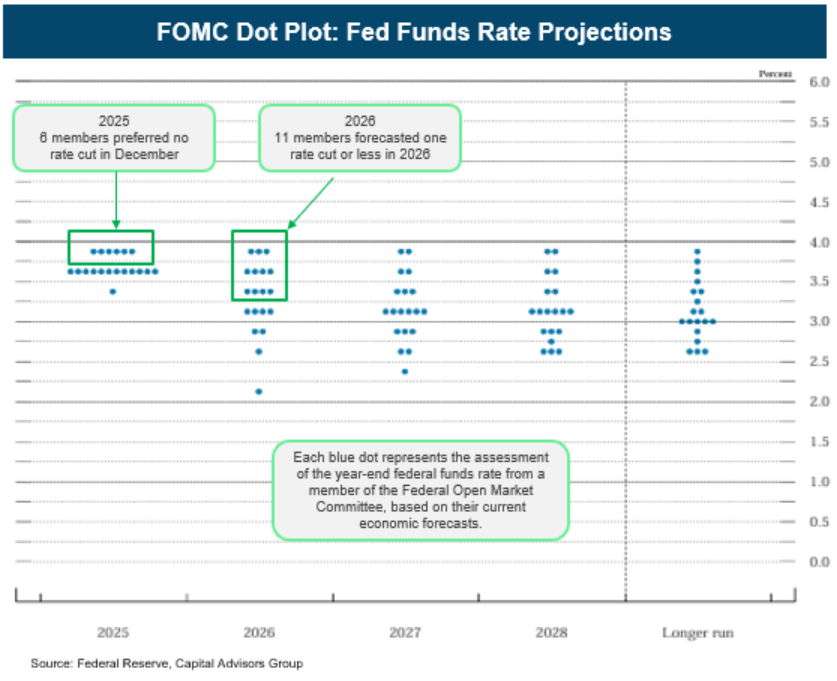

The December 10th FOMC meeting offered something for both hawks and doves, but it was the dot plot that most clearly highlighted a divided Federal Reserve.

From a hawkish perspective, the official FOMC statement reintroduced language last used in December 2024, just ahead of the Fed’s nine-month pause. By adding the phrase “the extent and timing of” in reference to future rate cuts, the Committee signaled optionality and laid the groundwork for a potential pause should the data warrant. The Fed also materially upgraded its 2026 GDP forecast, raising it from 1.8% to 2.3%, citing supportive fiscal policy, resilient consumer spending, and continued investment in artificial intelligence.

On the dovish side, Chair Powell expressed growing concern about the labor market, noting that “the downside risks to employment appear to have risen in recent months.” He added that labor market conditions have continued to gradually cool and have softened “maybe a touch more” than previously anticipated.

While the dot plot for 2026 and 2027 was effectively unchanged—still showing one 25 basis point cut in each year—the 2025 year-end dot plot underscored the ongoing divide within the Committee. Six participants placed their dots in the 3.75%–4.00% range, implying opposition to the 25 basis point cut at the December meeting. With only two members (Goolsbee and Schmid) formally dissenting, this suggests four additional “silent dissents” from Committee members.

Chair Powell addressed this division directly in his press conference, explaining that while all participants agree inflation remains too high and the labor market has softened, differences arise in how individual members weigh inflation risks versus labor market risks when setting policy.

Employment and Retail Sales: Takeaways from Delayed Data

Due to the recent government shutdown, several key economic releases for October and November were delayed. On December 16th, markets received the October and November employment reports, along with the October retail sales report. Below are the key takeaways:

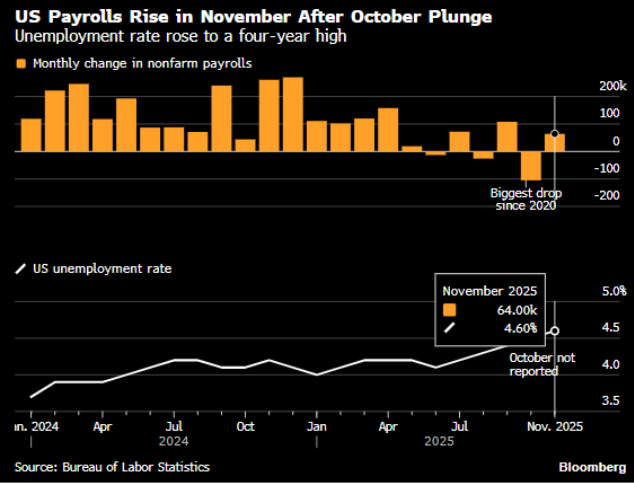

- November Employment Report: Nonfarm payroll growth exceeded expectations, rising by 64,000, while the unemployment rate increased to 4.6%, its highest level since September 2021. Importantly, part of the rise in unemployment reflected improving labor supply dynamics, as labor force participation increased with 323,000 individuals entering the workforce. A notable positive was the three-month average of private payroll growth, which improved to 75,000 jobs, a meaningful rebound from the May–July period that averaged just 15,000 jobs.

- October Employment Report: Nonfarm payrolls declined by 105,000, well below expectations, driven primarily by a 157,000 drop in government employment. This reflected the deferred impact of DOGE-related cuts to the federal workforce following the shutdown. An unemployment rate was not reported for October, as the household survey used to calculate it was not conducted during the shutdown.

- October Retail Sales Report: Retail sales data pointed to resilient consumer demand. Sales excluding autos and the Control Group both exceeded expectations, marking their strongest increases in four months. Headline retail sales were flat, weighed down by a 1.6% decline in motor vehicle sales, partly due to the expiration of federal tax incentives for electric vehicles. Eight of the thirteen retail categories posted gains, suggesting consumer spending improved in October, which is often viewed as the unofficial start of the holiday shopping season.

Markets were little changed following the releases, as investors largely viewed the data as noisy and distorted by shutdown-related timing issues. The Fed is likely to wait for additional clarity before adjusting its policy outlook. The next key data point will be the November CPI report on December 18th, which will be closely watched by inflation-focused members of the FOMC.

Rates, Risk Assets, and Fed Expectations

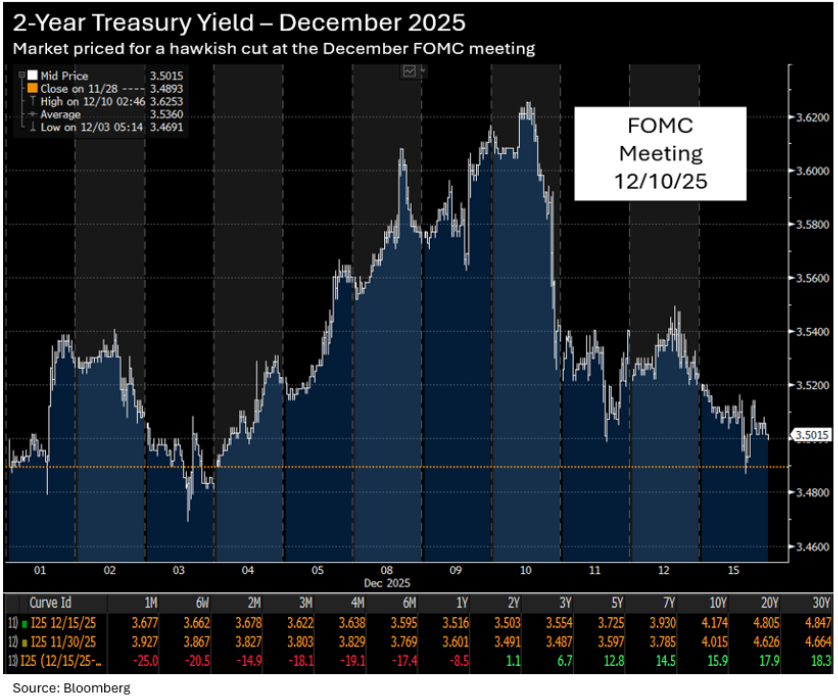

Entering December, markets were primarily focused on the upcoming FOMC meeting and had priced in what was widely viewed as a hawkish cut. This positioning pushed Treasury yields higher in the days leading up to the meeting, with the 2-year yield rising 12 basis points and the 10-year yield increasing 17 basis points ahead of the December 10th decision.

Following the FOMC meeting, Treasury yields declined across most of the curve, with the notable exception of the 20- and 30-year maturities. Longer-dated Treasuries have been more influenced by global bond market dynamics, where yields have generally trended higher. As of December 15th, yields were mixed: front-end yields have declined following the Fed’s 25 basis point rate cut, leaving the 2-year Treasury little changed on the month at approximately 3.50%, while the 10-year yield has risen 15 basis points to 4.174%.

Risk assets also delivered mixed performance. On the equity side, the Dow Jones Industrial Average is up 1.65% month-to-date, while the S&P 500 and Nasdaq are modestly lower, down 0.40% and 1.28%, respectively. In credit markets, spreads remain stable, with the Bloomberg Investment Grade Corporate Bond Index tightening by 1 basis point so far in December.

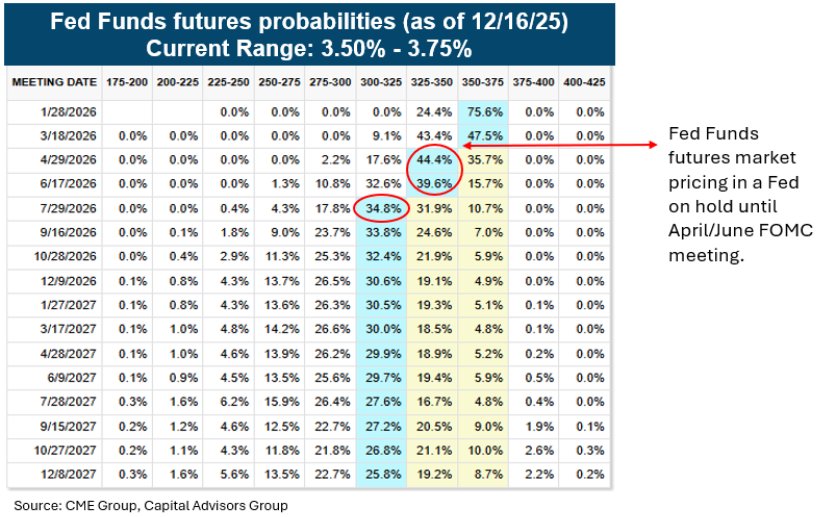

Looking ahead, the Fed funds futures market is currently pricing in a Federal Reserve that remains on hold until the April or June FOMC meeting. While the Fed’s projections point to 50 basis points of rate cuts over the next two years, market pricing implies that the same 50 basis points of easing will arrive within the next 12 months (see chart below).

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.