November Mid-Month Market Update

Heading Towards a Fed Santa Pause?

Hawkish commentary from the Federal Reserve has continued into November, with several officials pushing back against the idea of a rate cut at the December FOMC meeting. Recent remarks include:

- 11/12/25 – Boston Fed President Collins: “It will likely be appropriate to keep policy rates at their current level for some time.”

- 11/12/25 – Atlanta Fed President Bostic: I “favor keeping the funds rate steady until we see clear evidence that inflation is again moving meaningfully toward its 2% target.”

- 11/13/25 – St. Louis Fed President Musalem: “We need to proceed and tread with caution, because I think there’s limited room for further easing.”

With a growing number of Fed members signaling no urgency to ease policy, fed funds futures have recalibrated expectations. The probability of a December rate cut has fallen from nearly 90% to roughly a 50/50 split heading into the December 10th meeting.

Treasury markets have also repriced. Yields are higher across the curve since the October 29th FOMC meeting, with the 2-year yield up 11 bps to 3.608% and the 10-year yield up 17 bps to 4.149%.

Assessing the Shutdown’s Effects on GDP

Now that the government has ended the longest shutdown in history (43 days), attention is turning to its potential impact on the economy. Historically, economists estimate that each week of a shutdown reduces annualized quarterly GDP growth by roughly 0.1% to 0.2%. However, these effects are typically temporary, with activity rebounding in the subsequent quarter.

The Congressional Budget Office estimates that a six-week shutdown would have likely reduced GDP by 1.5%, followed by a 2.2% rebound in the first quarter of 2026 (see table below). Meanwhile, Bloomberg’s consensus forecast from 59 economists calls for Q4 GDP growth of 1.1% (see table below).

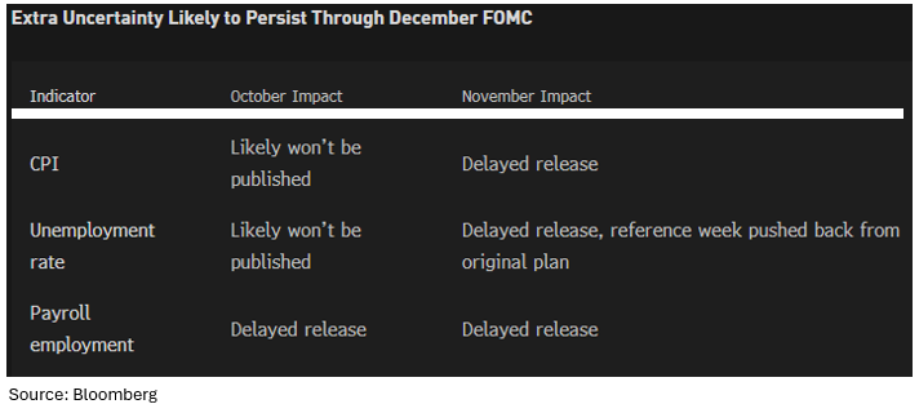

Expect Noise in Labor Market and Inflation Data Releases

The Bureau of Labor Statistics (BLS) has announced that it will release the September employment report on Thursday, November 20th. Data gathering for that report was largely completed before the government shutdown began, even though its scheduled release date fell after the shutdown started. The September CPI report was delayed but ultimately released last month.

There is, however, considerable uncertainty surrounding both the October CPI and employment data. On the labor front, we will likely receive an October non-farm payrolls figure, as that data is collected electronically. In contrast, the unemployment rate may not be published because it relies on manually conducted phone surveys.

On the inflation side, nearly 70% of CPI data is manually collected, with BLS staff physically visiting stores throughout the month. As a result, the more labor-intensive components of both the October labor market data and the October CPI may never be released.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.