As widely expected, the Federal Open Market Committee left the federal funds target range unchanged at 3.50%–3.75%. Key takeaways from the meeting are outlined below:

The June FOMC statement was significantly shortened, shrinking from 341 words in April to just 130 words, reflecting Chairman Warsh’s stated goal of making Fed communications shorter, simpler, and more focused on the facts (see statement below).

Consistent with our mid-month update, the Committee removed its easing bias and eliminated forward guidance, signaling a greater reliance on incoming economic data rather than pre-committing to a future policy path.

The Committee characterized the economy as expanding at a solid pace, highlighting strong productivity growth and capital investment—a likely reference to ongoing AI-related spending. At the same time, it offered a more measured assessment of the labor market, noting that “job gains have kept pace with the workforce,” while acknowledging that inflation has been pressured higher in part by energy-related supply shocks.

The statement concluded with the declaration that “The Committee will deliver price stability,” underscoring a heightened focus on the inflation side of the Fed’s dual mandate amid a labor market that remains broadly stable.

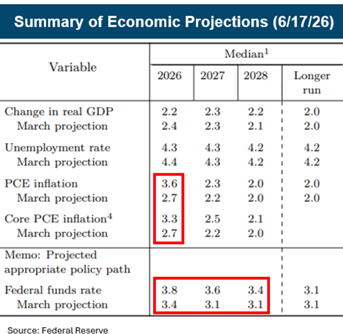

Summary of Economic Projections

The median federal funds rate projection now implies one 25 basis point rate hike by the end of 2026, followed by 25 basis point rate cuts in both 2027 and 2028.

FOMC participants significantly raised their inflation forecasts for 2026, with headline PCE inflation increasing from 2.7% to 3.7% and Core PCE inflation rising from 2.7% to 3.3%. Despite the upward revisions, both measures are projected to fall below 3% in 2027 as inflationary pressures gradually moderate.

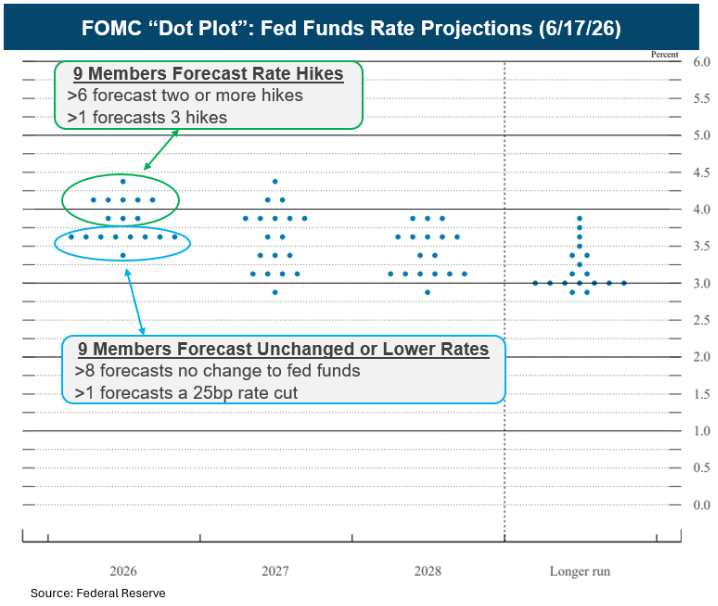

The dot plot revealed a divided Committee, with 9 participants projecting additional rate hikes and 9 participants expecting rates to remain unchanged or move lower. Notably, one participant did not submit a rate projection; Chairman Warsh later confirmed during the press conference that he was the non-participant, consistent with his long-standing reservations about the current structure of the Summary of Economic Projections.

Warsh Press Conference

In his opening remarks, Chairman Warsh delivered a strong message on inflation, noting that inflation has remained above the Fed’s 2% target for more than five years and emphasizing that the Committee is “unambiguous and unanimous” in its commitment to restoring price stability.

Warsh addressed the streamlined FOMC statement and the removal of forward guidance, which implies greater emphasis on incoming economic data rather than pre-committing to a future policy path.

He announced the creation of 5 task forces: Fed communications; Fed’s balance sheet policy; use and reliance on existing data sources; productivity and jobs in an era of transformation; and Fed’s inflation frameworks.

Consistent with his past criticisms of the Summary of Economic Projections (SEP), Warsh declined to submit his own dot plot and economic forecasts. However, he encouraged other FOMC participants to continue providing projections while noting that the communications task force will evaluate potential reforms to the SEP process.

When asked whether a rate cut was discussed during the meeting, Warsh acknowledged that there was one proposal on the table that was quite limited and “the group was unanimous and unambiguous” in rejecting it. One unanswered question is whether Warsh himself was the official who raised the proposal.

Warsh appeared to downplay the significance of the rate hike projections embedded in the dot plot, stating, “I didn’t hear a ton of conviction. What I heard was the kind of humility that I think we should have,” suggesting considerable uncertainty around the policy outlook.

Throughout the press conference, Warsh repeatedly highlighted the robust debate occurring within the Committee, referring to occasional “family fights” over policy issues while emphasizing that rigorous discussion and differing viewpoints ultimately strengthen the policymaking process.

Market Reaction

Treasury yields moved higher across the curve following the FOMC meeting, led by the 1- to 3-year sector as investors repriced expectations for a more restrictive policy path. In contrast, the long end remained relatively well anchored, with 20-year and 30-year Treasury yields little changed (see chart below).

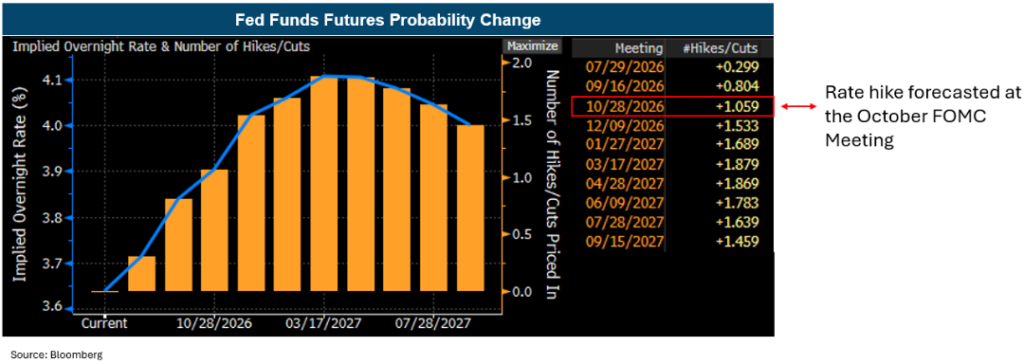

Fed funds futures shifted notably following the meeting and are now pricing in a 25 basis point rate hike at the October 28th FOMC meeting. The move reflects the market’s interpretation of the Fed’s more hawkish inflation outlook and Chairman Warsh’s strong emphasis on restoring price stability (see chart below).

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.

17 min read17 min read Key Takeaways If you’ve read the headlines lately, you might think the American consumer is finally buckling. In late May, The Wall Street Journal reported that the share of credit card balances at least 90 days past due climbed to 13.12% in the first quarter – the highest level since the aftermath…

7 min read7 min read Job Growth in June | AI Impact Limited The June employment report pointed to a labor market that continues to demonstrate resilience. Nonfarm payrolls increased by 172,000, while the three-month average payroll gain rose to 188,000, the strongest pace since 2024. The unemployment rate remained unchanged at 4.3%, although on an unrounded basis…

5 min read5 min read Economic Data Pushes Out Potential Rate Hike Recent labor market and inflation data prompted the fed funds futures market to fully price in a rate hike by December, pushed back from expectations for a September hike earlier this month. Despite the shift, the broader consensus among economists continues to be that the FOMC is more likely to remain on hold throughout 2026 rather than raise…

5 min read5 min read Diverging Views on Monetary Policy Path Although both the Federal Reserve’s June projections and the fed funds futures market are currently signaling the possibility of a rate hike in 2026 (see first chart below), the broader consensus among economists remains that the Fed will likely stay on hold. One of the more notable takeaways from the…

10 min read10 min read Key Takeaways Shifting Expectations: How the Middle East Conflict Altered the Fed’s Rate Path The conflict in the Middle East has thrown a wrench into the Federal Reserve’s cutting cycle. Prior to the initial attacks on Iran in March, the case for cutting rates in 2026 was strong: Then, the unprecedented closure…

7 min read7 min read Job Growth in June | AI Impact Limited The June employment report pointed to a labor market that continues to demonstrate resilience. Nonfarm payrolls increased by 172,000, while the three-month average payroll gain rose to 188,000, the strongest pace since 2024. The unemployment rate remained unchanged at 4.3%, although on an unrounded basis…