June Month-End Market Update

Diverging Views on Monetary Policy Path

Although both the Federal Reserve’s June projections and the fed funds futures market are currently signaling the possibility of a rate hike in 2026 (see first chart below), the broader consensus among economists remains that the Fed will likely stay on hold. One of the more notable takeaways from the June FOMC meeting was the degree of division within the Committee itself. Of the 18 policymakers who submitted projections, nine penciled in at least one rate hike, while the other nine projected either no change in rates or eventual rate cuts. The median projection currently reflects one rate hike in 2026 followed by rate cuts in 2027 and 2028.

It is worth noting that Fed Chair Warsh did not submit a policy-rate projection. Had he done so, his forecast could have shifted the median outlook toward no rate hike in 2026, potentially resulting in a less hawkish interpretation of the Committee’s policy stance.

In contrast, a late-June survey of 40–50 economists (below) paints a notably different picture:

- Row 4: US 2-Year: The 2-year Treasury yield is expected to decline over the remainder of 2026, ending the year at approximately 3.85%, well below current levels.

- Row 6: Fed Funds Rate – Upper Bound: Forecasts for the federal funds rate upper bound, currently 3.75%, imply that the Fed’s next move will be rate cuts rather than rate hikes.

Taken together, these forecasts suggest that while policymakers remain concerned about inflation risks, most economists expect economic growth to slow sufficiently to keep the Fed on hold before ultimately easing policy rather than tightening further.

Strait of Hormuz Reopens, but Risks Remain

The conflict with Iran has been one of the dominant market drivers of 2026, influencing inflation expectations, energy prices, and the outlook for monetary policy. A major step toward de-escalation occurred on June 17th, when the U.S. and Iran signed a Memorandum of Understanding that included the reopening of the Strait of Hormuz. While shipping traffic remains below pre-war levels and security concerns persist, oil markets have responded favorably, with Brent crude falling back to levels seen before the conflict began, including a 38.4% fall in the second quarter, the biggest quarterly decline since the pandemic. However, Brent remains up over 19% year-to-date.

Inflation Expectations

The Federal Reserve’s preferred inflation gauge, Personal Consumption Expenditures (PCE), delivered a mixed report for May. Headline PCE rose 0.4%, coming in below expectations, but the increase was still enough to push the year-over-year rate back above 4% to 4.1%, its highest level since 2023. Core PCE, which excludes the more volatile food and energy components, increased 0.3% during the month, lifting the annual rate to 3.4%, the highest reading since October 2023.

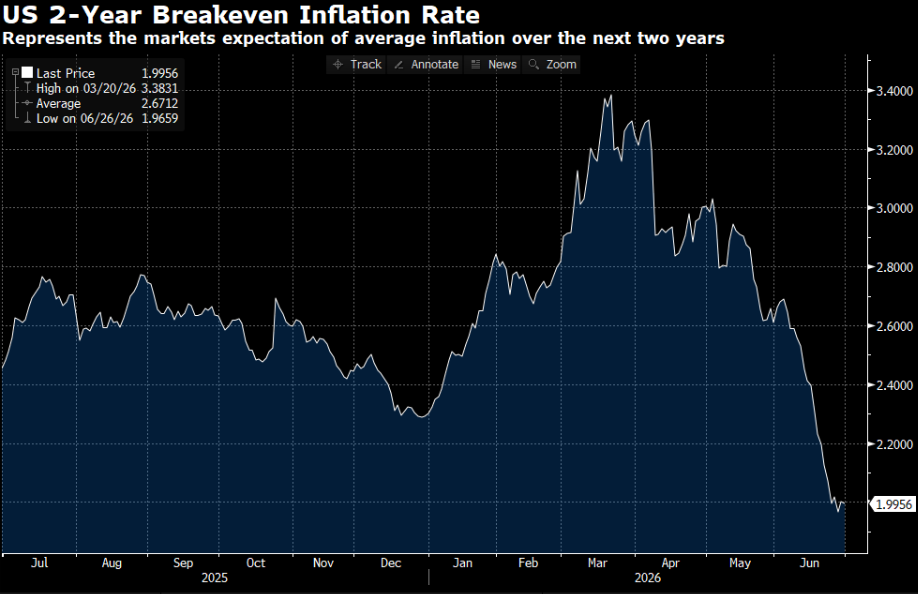

Looking ahead, inflation expectations have begun to moderate. The 2-year breakeven inflation rate, a market-based measure of expected inflation, has fallen sharply from approximately 3.4% in March to below 2.0% by the end of June (see chart below). A key driver of this decline has been easing geopolitical tensions in the Middle East, particularly the progress toward a resolution of the conflict with Iran, which has contributed to lower energy prices and reduced concerns about a prolonged inflation shock.

While current inflation readings remain elevated, the recent decline in market-based inflation expectations suggests investors are increasingly viewing the energy-driven inflation surge as temporary rather than the beginning of a broader and more persistent inflation cycle.

2026 First Half Recap

The first half of 2026 was marked by rising Treasury yields, resilient economic growth, and strong performance across risk assets. Inflation concerns associated with the conflict in Iran pushed yields higher and led markets to reprice the expected path of Fed policy. Despite the rise in rates, equities posted solid gains and credit spreads tightened, reflecting continued confidence in corporate fundamentals and sustained momentum for AI-driven investment.

- Treasuries: Treasury yields rose across the curve during the first half of the year, led by the 2-year Treasury yield, which increased 70 basis points (see chart below). Most of the move occurred following the onset of the conflict with Iran, as higher energy prices fueled inflation concerns and caused markets to scale back expectations for future Fed rate cuts.

- Equities: All three major equity indexes advanced during the first half of 2026. The Dow Jones Industrial Average gained 9.76%, the S&P 500 rose 10.19%, and the Nasdaq advanced 13.14% on a total return basis. The second quarter marked the strongest quarterly performance for both the S&P 500 (+15.20%) and the Nasdaq (+21.60%) since 2020, supported by resilient economic data, strong corporate earnings, and continued enthusiasm surrounding AI-related investments.

- Credit: Corporate credit markets remained exceptionally resilient despite higher Treasury yields. Investment-grade credit spreads tightened across both front-end and longer-duration indexes, reflecting strong investor demand and healthy corporate fundamentals. New issuance remained robust, with approximately $200 billion of investment-grade bonds priced in June alone—the largest June issuance volume on record—led by landmark transactions from Nvidia and SpaceX totaling approximately $25 billion.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.