June Mid-Month Market Update

Job Growth in June | AI Impact Limited

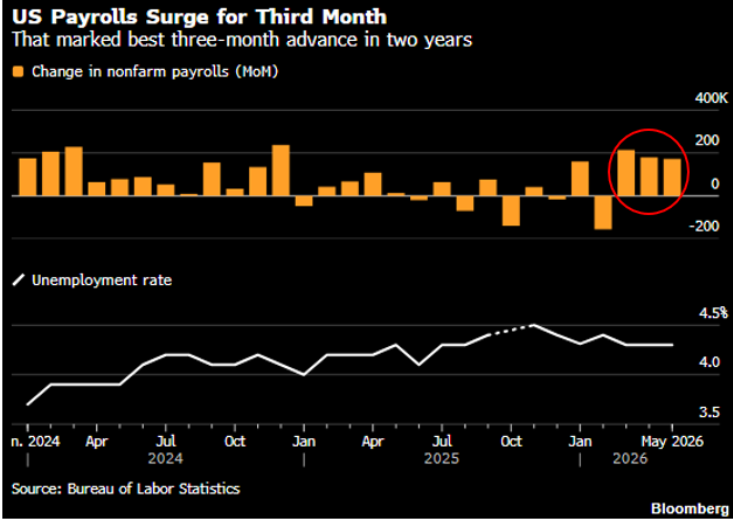

The June employment report pointed to a labor market that continues to demonstrate resilience. Nonfarm payrolls increased by 172,000, while the three-month average payroll gain rose to 188,000, the strongest pace since 2024. The unemployment rate remained unchanged at 4.3%, although on an unrounded basis it improved slightly, declining from 4.337% to 4.296%.

Another encouraging aspect of the report was the direction of revisions. In contrast to the downward revisions that have characterized many recent employment releases, the June report included a combined 93,000 upward revision to the prior two months. May payroll growth was revised higher from 115,000 to 179,000, marking the first positive two-month net revision since June 2025 and the largest upward revision in 15 months.

The ongoing FIFA World Cup also appears to have provided a boost to hiring activity. The Leisure and Hospitality sector added 70,000 jobs, the largest monthly increase in more than three years, reflecting increased demand tied to travel, tourism, and event-related spending.

Bottom Line: The June employment report suggests labor market conditions remain firmer than many had anticipated. Strong payroll growth, meaningful upward revisions, and a stable unemployment rate are likely to reinforce the view that the Fed can remain patient as it assesses the path of inflation and economic growth.

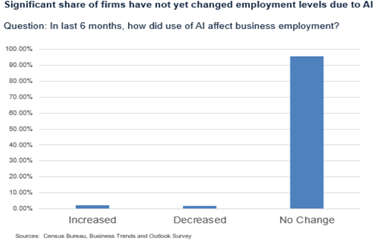

One of the key economic debates this year has centered on the potential impact of artificial intelligence (AI) on employment. While concerns about widespread job displacement have garnered significant attention, the available data suggests AI’s effect on the labor market has been limited thus far. According to the U.S. Census Bureau’s Business Trends and Outlook Survey, approximately 96% of firms that have adopted AI reported no change in overall staffing levels, indicating that AI is being used primarily to enhance worker productivity, improve existing processes, and expand organizational capabilities rather than replace employees (see chart below).

This finding is consistent with broader labor market indicators, which continue to show labor demand exceeding labor supply. While AI is likely to reshape the nature of work over time, recent evidence suggests its current role is largely complementary to human labor rather than a substitute for it.

Higher Energy Prices Pushes Inflation to a 3-Year High

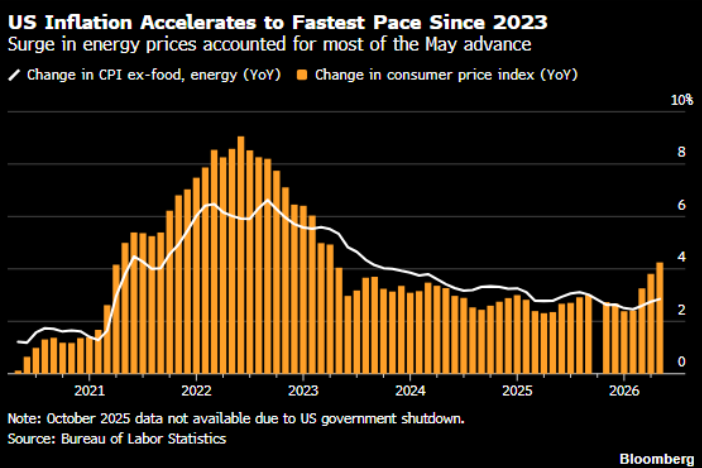

The May Consumer Price Index (CPI) report delivered a mixed inflation picture. Headline CPI rose 0.5%, in line with expectations, but marked a moderation from March’s 0.9% increase, which was largely driven by the surge in oil prices following the conflict with Iran. The energy index increased 3.9% during the month and accounted for more than 60% of the overall rise in consumer prices. Gasoline prices rose 7% in May and are now up more than 40% from a year ago.

The good news is that gasoline prices have declined modestly in recent weeks. Adding to that optimism, reports over the weekend indicated that the United States and Iran have reached a framework agreement aimed at ending the conflict and reopening the Strait of Hormuz. The agreement is expected to be formally signed in Switzerland this Friday. While the deal still faces potential challenges—including opposition from Israel—the market reaction has been positive, with oil prices moving lower on the news. If sustained, lower energy prices should help ease inflationary pressures and provide some relief in upcoming inflation reports.

Core CPI, which excludes food and energy, provided a more encouraging signal. Core prices rose just 0.2%, coming in below expectations and suggesting that underlying inflation pressures remain relatively contained. The stability in core inflation should give the Federal Reserve flexibility to remain on hold in the near term, as the recent acceleration in headline inflation appears to be driven primarily by energy prices rather than broad-based price pressures across the economy.

Investment Grade Issuance Tops $1 trillion

Treasury yields were little changed through June 12, before reports emerged over the weekend that the United States and Iran had reached an agreement to end the conflict and reopen the Strait of Hormuz. Front-end yields out to two months remained largely unchanged, while maturities from three months to twenty years moved less than 10 basis points during the period (see chart below). As a result, the yield levels shown below do not reflect any potential market reaction to the agreement. While the Treasury market was relatively quiet through mid-month, investor attention shifted toward developments in the equity and credit markets.

In equities, the spotlight was on SpaceX, which completed the largest IPO in history. The month also saw both Anthropic and OpenAI announce plans to go public within days of each other, further fueling enthusiasm around artificial intelligence-related investments. Despite the excitement surrounding AI, equity market performance was mixed. The Dow Jones Industrial Average posted a modest gain of 0.3%, while the S&P 500 declined 2.0% and the Nasdaq fell 4.0% during the first half of the month.

Credit markets continued to demonstrate remarkable strength. Investment-grade corporate bond issuance surpassed $1 trillion in early June, reaching that milestone at the fastest pace since 2020. The surge in issuance has been driven in part by elevated capital spending needs related to AI infrastructure and technology investment. For perspective, investment-grade issuance did not exceed $1 trillion until August in 2025, and prior to 2020, that threshold was typically not reached until much later in the year. Despite the increase in supply, investment-grade credit spreads remain tighter on a year-to-date basis, underscoring continued investor demand and the resilience of the corporate bond market.

Week Ahead: First FOMC Meeting Under Warsh

This Tuesday and Wednesday will mark the first FOMC meeting chaired by newly appointed Fed Chair Kevin Warsh. One of the key areas of focus will be whether the Committee removes its longstanding easing bias from the official policy statement. Consensus expectations are for the FOMC to revise the phrase, “In considering the extent and timing of additional adjustments to the target range for the federal funds rate,” as the current language implies that the next policy move is more likely to be a rate cut than a hike.

The Committee will also release an updated Summary of Economic Projections (SEP). In its previous projections, the Fed anticipated one 25-basis-point rate cut in 2026 and another in 2027. Prior to the weekend, market expectations were that policymakers would remove the projected 2026 rate cut, with some participants potentially penciling in rate hikes given persistent inflation pressures. However, the reported agreement between the United States and Iran introduces a potentially important new variable. If the agreement leads to lower oil prices and easing inflation concerns, it will be interesting to see whether and how those developments influence the Committee’s economic and policy outlook.

Warsh’s press conference will be closely watched for insight into his broader monetary policy framework. Investors will be looking for clues regarding his preferred inflation measures, views on forward guidance, frequency of Fed communications, and perspective on the dot plot itself. Several economists have speculated that Warsh may choose not to submit a policy-rate projection, reflecting his long-standing skepticism toward forward guidance and the signaling effects of the dot plot.

At his first meeting as Chair, Warsh is expected to strike a balanced and data-dependent tone. While he is unlikely to signal support for near-term rate cuts, he may also avoid explicitly endorsing future rate hikes. The reported U.S.-Iran agreement has the potential to ease one of the Fed’s primary inflation concerns by lowering energy prices and reducing the risk of a broader inflation shock. Given the significant shift in Fed leadership and the uncertainty surrounding the policy outlook, his press conference is likely to be one of the most closely watched Fed events of the year.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.