May Month-End Market Update

Core PCE Indicates Broadening Price Pressures

The Fed’s preferred inflation gauge, Core Personal Consumption Expenditures (PCE), delivered both encouraging and concerning signals in the April report. The good news was that monthly inflation readings came in below expectations, with headline PCE rising 0.4% and Core PCE increasing 0.2%. While gasoline and other energy prices rose 5.5% during the month, adding approximately 13 basis points to headline PCE, core nondurable goods prices were largely unchanged, helping to contain broader inflation pressures.

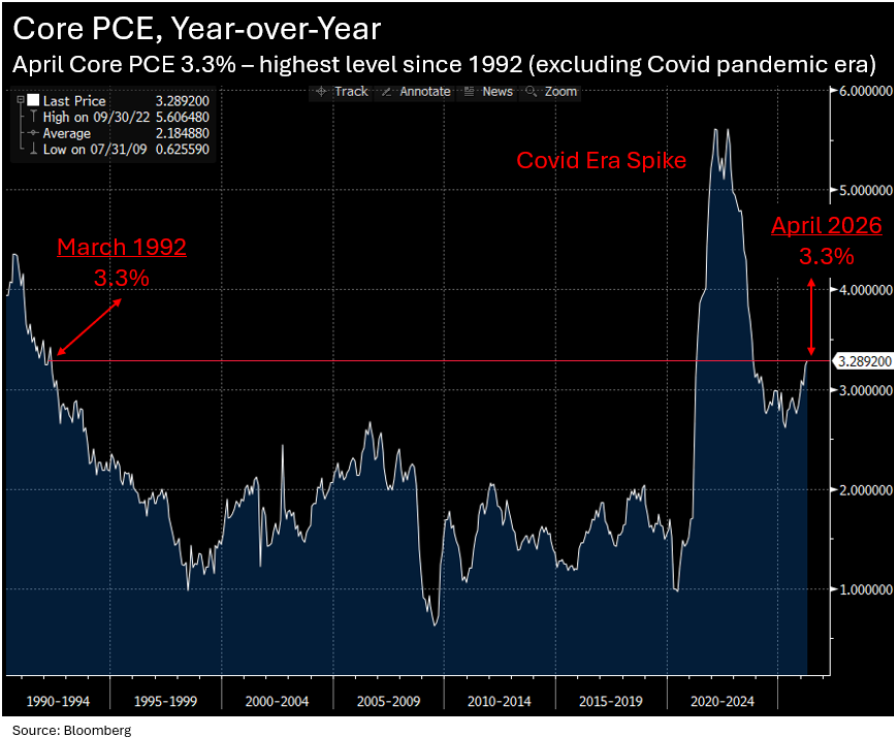

The less encouraging news is that the year-over-year Core PCE rate has climbed to 3.3%. Excluding the pandemic-era inflation surge, this represents the highest reading since 1992 (see chart below). In addition, both the 3-month and 6-month annualized Core PCE measures are running at 3.8%, suggesting that inflation pressures are extending beyond the temporary effects of higher energy prices. This persistence in underlying inflation helps explain the increasingly hawkish tone from several Fed policymakers in recent months.

Looking ahead, inflation is expected to remain above 3% through the remainder of the year, with forecasters not anticipating a return to the Fed’s 2% target range until the second quarter of 2027 (see chart below). The key question for markets is whether inflation pressures broaden further or begin to moderate as the effects of the energy shock fade.

A Key Fed Dove Now Leans Hawkish

Fed Governor Christopher Waller has been one of the most consistently dovish members of the FOMC. At the January 2026 meeting, Waller joined Governor Stephen Miran in dissenting in favor of a 25 basis point rate cut. However, more recent comments suggest a notable shift in tone. In a May 22nd speech, Waller joined a growing number of Fed officials expressing support for removing the current easing bias from the FOMC’s policy statement, signaling a move toward a more neutral policy stance.

Perhaps more importantly, Waller also acknowledged the possibility of future rate hikes. While he stated that keeping the federal funds rate within its current 3.50%–3.75% range is likely the appropriate course for the foreseeable future, he added that he can “no longer rule out rate hikes further down the road if inflation does not abate soon.” His remarks underscore the Fed’s increasing focus on persistent inflation pressures and highlight the broader hawkish shift taking place within the Committee.

A Memorial Month for Markets

As we honored the military personnel who made the ultimate sacrifice in service to our country this Memorial Day, markets also experienced a memorable month of May. All three major equity indices closed at record highs, while both stocks and bonds rallied into month-end on growing optimism that a path toward ending the Iran conflict may be emerging.

- Treasuries: Treasury yields moved higher across the curve during May, reflecting persistent inflation concerns and a hawkish repricing of Fed expectations. However, yields declined during the final week of the month on optimism surrounding a potential Iran agreement. The 2-year and 3-year Treasury yields remained above the 4% threshold for a second consecutive month (see chart below), although both fell approximately 12 basis points during the final week of May. On a year-to-date basis, the 2-year Treasury yield has risen 53 basis points as markets have steadily priced out rate cuts over the next two years.

- Equities: The S&P 500, Nasdaq, and Dow Jones Industrial Average all closed at record highs during May. The S&P 500 recorded its ninth consecutive week of gains, supported by strong corporate earnings and improving investor sentiment. The Nasdaq surged 25% over the past two months, marking its strongest two-month advance in 24 years.

- Corporate Bonds: Credit markets continued to strengthen, with spreads tightening across both investment-grade and high-yield sectors. The Bloomberg 1–3 Year and 1–30 Year Credit Indexes each tightened by approximately 5 basis points during the month, while high-yield spreads narrowed by 11 basis points. Market-based measures of risk also improved. The CDX Investment Grade Index, often referred to as the corporate credit market’s “fear gauge”, declined to its lowest level in more than three months (see chart below). Similarly, the MOVE Index, a widely followed measure of Treasury market volatility and often described as the bond market’s equivalent of the VIX, also moved lower, signaling reduced interest-rate uncertainty and improving credit market conditions (see chart below).

- Oil: Oil prices fell sharply during May on hopes that a preliminary agreement will ultimately lead to the end of the war with Iran and reduce concerns about oil supply disruptions. WTI crude declined 11.9% to $87 per barrel (see chart below) while Brent crude fell 19.3% to $92 per barrel, which is the largest monthly decline since March 2020 at the onset of the Covid-19 pandemic.

Bottom Line: Despite higher interest rates and ongoing geopolitical uncertainty, investor sentiment improved materially during May. Record equity prices, tighter credit spreads, lower volatility measures, and declining oil prices all reflected growing confidence that geopolitical risks may begin to moderate in the months ahead.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.