A New Fed Chair, A New Direction?

What Kevin Warsh’s Confirmation Signals for Monetary Policy and Market Expectations

Key Takeaways

- Institutional shift over policy shock: Warsh’s impact is more likely to come from reshaping how the Fed operates than from immediate rate changes.

- Rates stay constrained: A hawkish FOMC may limit near-term easing, supporting a “higher-for-longer” rate backdrop.

- Less Fed transparency ahead: Communication may become more restrained, with reduced forward guidance and potential changes to tools like the Dot Plot.

- Balance sheet and regulation in focus: The most durable impact may come from regulatory reform and balance sheet policy, where alignment with Vice Chair Michelle Bowman could matter.

Kevin Warsh is now officially Chair of the Federal Reserve after being confirmed by the Senate and sworn in by President Trump. The former Fed Governor takes the seat amid a tricky backdrop characterized by rising oil prices, a lethargic labor market, and a Federal Open Market Committee (FOMC) that has overshot its inflation target for more than 60 consecutive months.

So, what should markets make of the new Chair and his potential impact on monetary policy?

There are several areas where Warsh could leave his mark, while others may prove more difficult as he faces stern opposition from the current makeup of the FOMC.

Interest Rates

This is the area where Warsh’s views have been most scrutinized, but perhaps least understood.

During his tenure as Fed Governor from 2006-2011, Warsh was widely viewed as an inflation hawk. More recently, however, his public commentary has struck a more dovish tone. In several speeches, he has pointed to the potential disinflationary effects of an AI-driven productivity boom.

At the same time, Warsh has argued that the Fed should be held culpable for the persistent inflationary overshoot during the post-COVID era.

These diverging views can appear difficult to reconcile, and may reveal less about how Warsh will conduct monetary policy in practice.

A Hawkish FOMC Could Limit Early Policy Shifts

Warsh also inherits an FOMC with a decidedly hawkish tilt.

The Fed’s April decision to hold rates steady resulted in a record four dissents, the largest number in more than 30 years. Importantly, most of the dissents were not aimed at the rate decision itself, but rather at the Committee’s preference to retain an easing bias within the policy statement.

Historically, the Fed has operated as a consensus-driven organization — a spirit fostered originally by Ben Bernanke and expounded on by Janet Yellen and Jerome Powell. Given the current tone of the Committee, it may be difficult to imagine the new Chair pursuing an easier policy out of the gate if broader consensus continues pushing in the opposite direction.

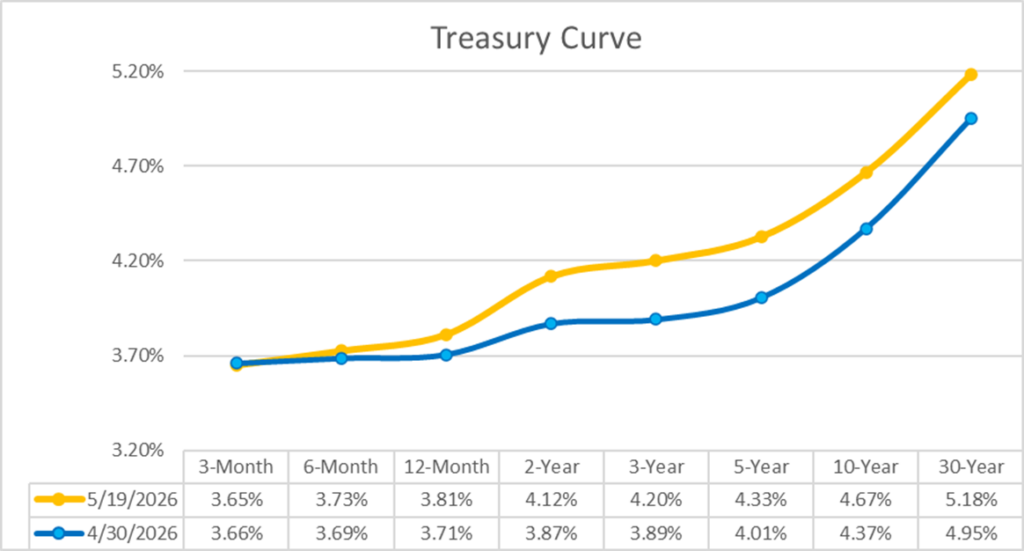

Market Reaction Signals Expectations for Higher-for-Longer Rates

In this context, the market reaction to Warsh’s nomination makes sense.

Following the announcement, the Treasury curve bear-steepened, with short-term rates moving modestly higher and long-term yields rising more sharply. The 30-year Treasury yield notably touched a recent high of 5.17%.

Markets appear to be pricing in two key expectations:

- The Fed is less likely to cut rates in the near term

- Longer-term inflation tolerance may be rising

For investors and treasury teams, the takeaway is that “higher for longer” rate expectations may remain intact, even under new Fed leadership.

Source: Bloomberg

Fed Communication Could Shift Under Warsh

Warsh has consistently espoused a preference for less communication from the Federal Reserve.

Over the years, he has floated several potential changes to Fed communication practices, including:

- Reducing the number of FOMC meetings

- Curtailing (if not outright eliminating) the Summary of Economic Projections (SEP)

- Limiting meeting transcripts to cover only portions of policy discussions

The goal behind these proposals appear to be twofold:

- To reduce what Warsh views as excessive forward guidance that can risk anchoring market expectations

- To foster a culture of openness and dissent within the FOMC, where minority opinions can be aired during meetings rather than through public comments afterward

A Push for Less Forward Guidance

Many of Warsh’s views on transparency trace back to a 2014 study he conducted for the Bank of England focused on the institution’s communication and meeting procedures.

One of his recommendations was to “turn off the tape recorder” during the initial round of deliberations, recording only the decision-making and voting portions. The Bank of England (BOE) ultimately adopted the proposal.

If implemented at the Fed, similar changes would mark a meaningful break from the institution’s long-running trend toward greater transparency.

Could the Fed Eliminate the Dot Plot?

One of the most notable possibilities is the elimination of the Fed’s so-called “Dot Plot”, which shows policymakers’ expectations for future interest rates.

Removing the Dot Plot could increase volatility in market-implied rate expectations, particularly during periods of economic uncertainty.

That’s not to say the idea is without merit.

The Dot Plot was first introduced in 2012 when short-term interest rates were stuck at 0%. At the same time, it served as an additional form of forward guidance by signaling that short rates would remain at or near 0% for a prolonged period of time, effectively acting as a qualitative stimulus in lieu of additional cuts.

With interest rates now well above zero, some policymakers and market participants argue that the tool has outlived its usefulness.

Balance Sheet & Regulatory Policy

Balance sheet policy and bank regulation are key areas where Warsh may be most likely to leave a substantive mark.

He has long argued that the Fed’s footprint — both in terms of financial markets and in the regulatory system — has become too large. In many ways, that view aligns with a prevailing direction of central bank thought.

Following years of tighter bank regulation and expanding balance sheets through Quantitative Easing (QE), many central banks are searching for ways to operate more efficiently and reduce excess regulatory burden.

Potential Policy Changes Under Warsh

Several policy shifts could emerge under Warsh’s leadership:

Restarting Quantitative Tightening (QT)

The Fed ended quantitative tightening (QT) in December and has since resumed growing its balance sheet through purchases of Treasury bills and notes with less than 3 years to maturity.

Warsh could propose:

- Ending those purchases

- Restarting balance sheet runoff

- Actively selling agency mortgage-backed securities (MBS) holdings

Such actions could serve dual purposes:

- Shrinking the Fed’s balance sheet

- Accelerating the transition toward a Treasury-only portfolio

Reworking Liquidity Rules and the Discount Window

Warsh has also floated the idea of reducing the stigma associated with the Fed’s Discount Window and incentivizing greater usage of the Fed’s lending facilities by tying them to bank liquidity reforms.

The reforms would allow banks to count their Fed borrowing capacity towards Liquidity Coverage Ratio (LCR) requirements, reducing banks’ incentive to hoard reserves and, in turn, support a smaller Fed balance sheet.

Support from Fed Leadership

In these efforts, Warsh would likely have an important ally in Fed Vice Chair of Supervision Michelle Bowman.

Together, they would hold two of the most important seats on the Board for regulatory matters, potentially allowing certain policy and regulatory changes to move forward in relatively short order.

Conclusion

Kevin Warsh arrives at the Fed at a pivotal and challenging moment.

His tenure will likely be defined not only by the macroeconomic backdrop he inherits — persistent inflation, a complex labor market, and heightened political scrutiny — but also by his willingness and ability to reshape an institution historically resistant to rapid change.

A Fed Chair Facing Structural Constraints

On interest rates, the current hawkish composition of the FOMC will likely constrain any dovish impulses Warsh may hold. Financial markets have already begun repricing expectations accordingly, reflecting a growing belief that rates could remain higher for longer.

A Potential Shift in Fed Communication Strategy

On communication policy, Warsh’s preference for less forward guidance and greater internal deliberation represents a genuine philosophical shift for the Fed.

If implemented, these changes could meaningfully alter how markets interpret Fed signals.

Balance Sheet and Regulatory Reform Could Be His Biggest Legacy

Balance sheet policy and bank regulation may become the areas where Warsh leaves the clearest and most lasting mark.

His alignment with Vice Chair Bowman gives him a potentially powerful ally in advancing regulatory reform, reducing the Fed’s market footprint, and reshaping liquidity policy.

A Gradual Reorientation of the Federal Reserve

Ultimately, Warsh’s chairmanship may be best understood not as a sharp policy pivot, but as a gradual institutional reorientation — one that pulls the Fed away from the hyper-transparent, heavily interventionist posture of the post-GFC era toward a leaner, more deliberative central bank.

Bottom line: A Warsh-led Fed may mean less forward guidance and more interest rate volatility, reinforcing the need to stay alert to Fed communication and prepared for a less predictable rate environment.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.