May Mid-Month Market Update

Labor Stability and Firm Inflation Keep the Fed Cautious

Labor Market: The April employment report pointed to continued stability in the labor market, with nonfarm payrolls exceeding expectations for the second consecutive month (+115,000 in April following +185,000 in March). This marked the first back-to-back monthly job gains since May 2025 and remains well above the Federal Reserve’s estimated breakeven pace of roughly 10,000 jobs per month needed to keep the unemployment rate stable.

However, job growth remains heavily concentrated in the healthcare sector, suggesting underlying hiring trends across the broader economy remain subdued. The unemployment rate held steady at 4.3%, though on an unrounded basis it increased from 4.256% to 4.337%. Meanwhile, the labor force participation rate, the share of the population either working or actively seeking employment, declined for the fifth consecutive month, falling to its lowest level since October 2021.

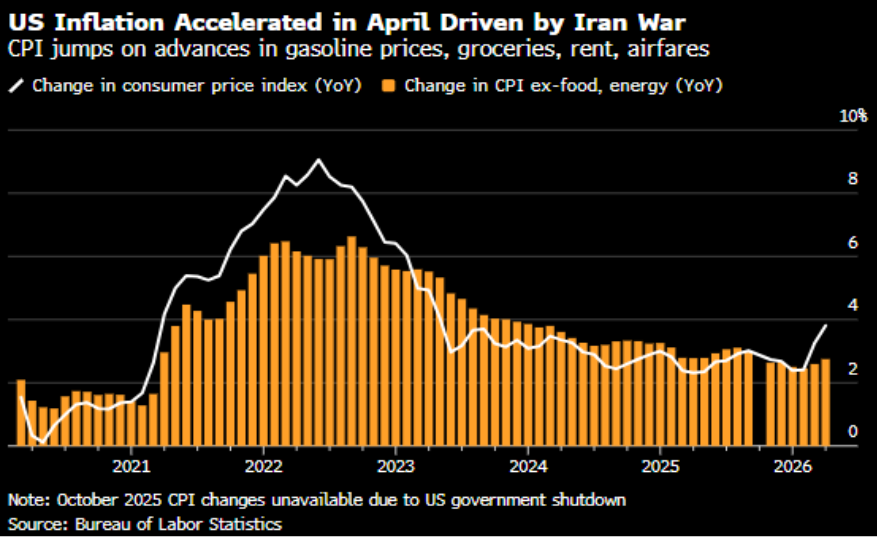

Inflation: The April Consumer Price Index (CPI) report highlighted the broader inflationary effects stemming from the conflict in the Middle East. Rising energy costs have increasingly filtered through to other categories, including groceries, rents, delivery services, and airfares, contributing to Core CPI rising 0.4%, which was above expectations, while headline CPI increased 0.6%, in-line with forecasts.

Although part of the stronger core reading reflected a statistical distortion tied to housing costs, the breadth of price increases remains notable. Grocery prices posted their largest monthly increase since 2022, underscoring the growing impact of higher transportation and energy costs on consumers. On a year-over-year basis, headline CPI accelerated to 3.8%, the highest level in three years, while Core CPI rose to 2.8%, roughly in line with the average core inflation pace seen throughout 2025.

Incoming Fed Chair nominee Kevin Warsh has indicated a preference for focusing on trimmed inflation measures, which also pointed to firmer underlying price pressures. The Federal Reserve Bank of Cleveland’s trimmed mean CPI rose 0.4% in April, marking its sharpest monthly increase since 2024.

Consumer: April retail sales data continued to point to a resilient consumer. Both headline retail sales and the Control Group, which feeds directly into GDP calculations, rose 0.5% during the month. On a three-month annualized basis, the Control Group accelerated to 7.9% from 5.7%, marking the strongest pace since June 2022.

The gains were broad-based, with 9 of 13 categories posting increases. Notably, restaurant and bar spending, the only services-related category within the report, rose 0.6%, suggesting consumers continue to spend on discretionary experiences despite pressure on household budgets from higher energy prices.

Looking ahead, however, there are emerging signs of strain. The personal savings rate declined in March to its lowest level in three years, while the burden of higher prices is increasingly being felt by lower-income consumers, not only at the gas pump, but also through rising grocery costs.

Treasury Yields Rise as Risk Assets Remain Resilient

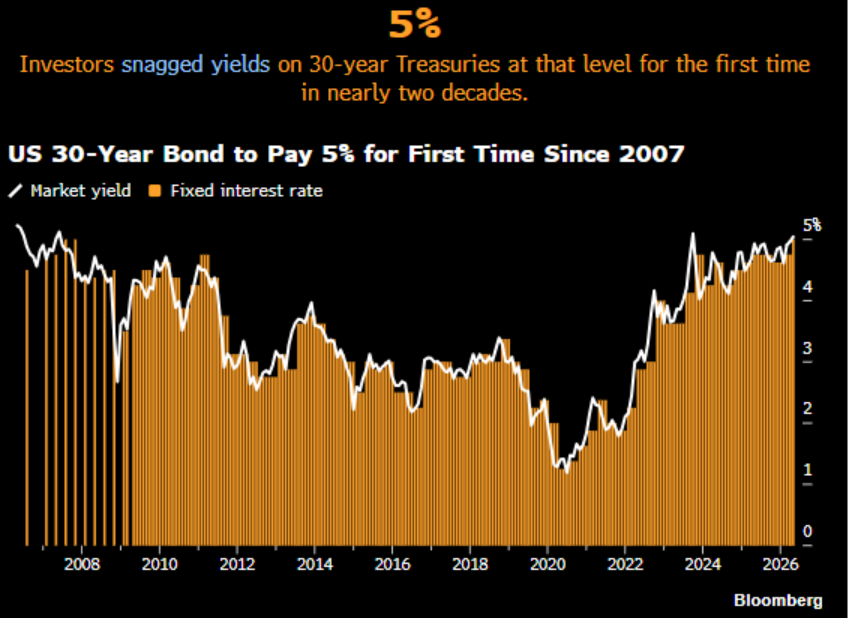

The move higher in Treasury yields during May has been notable, with rates rising across the curve and reaching several key milestones. For the first time since 2007, the 30-year Treasury bond was auctioned with a coupon above 5% (see chart below). Meanwhile, both the 2-year and 3-year Treasury yields moved back above 4%, while the 10-year Treasury yield climbed to 4.593%, its highest closing level since February 2025 (see chart below).

The rise in yields has been driven in part by higher oil prices and increasing inflation expectations in the U.S., but global fixed income markets have also contributed to the move. Government bond yields in both Japan and the United Kingdom have moved higher as renewed inflation concerns, combined with widening government deficits, have increased expectations for elevated sovereign debt issuance.

Despite the rise in rates, risk assets have remained resilient. The S&P 500 surpassed 7,500 for the first time ever, while the Nasdaq is up over 5% this month. Credit markets continued to strengthen. Spreads, as measured by the Bloomberg Credit Indexes, tightened across both investment grade and high yield sectors during the month.

FOMC Update: Markets Await Warsh’s Policy Direction

On May 13, Kevin Warsh was confirmed by the Senate as the 17th Chair of the Federal Reserve and is set to be sworn in on Friday May 22nd at the White House by President Trump. Warsh’s first FOMC meeting as Chair will take place on June 16–17.

Warsh will inherit a Committee that has recently shifted in a more hawkish direction, with growing opposition to maintaining an easing bias within the official FOMC statement. Additional dissents are possible in upcoming meetings if the Committee does not move toward more neutral policy guidance.

He will also take office at a time when markets have materially repriced the path of monetary policy. Fed funds futures are currently implying that the next move by the Fed could be a 25 basis point rate hike in January (see chart below), reflecting persistent inflation concerns tied to higher energy prices and geopolitical uncertainty.

While there will be several key economic releases before the June meeting, markets are already focused on Warsh’s first press conference as Chair. Investors will be watching closely to see whether he adopts a more dovish tone similar to Governor Stephen Miran, who has dissented repeatedly in favor of rate cuts, or instead positions himself as a more centrist and data-dependent policymaker seeking to balance inflation and growth risks.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.