What’s Driving Money Market Volatility—Is Reserve Scarcity Driving the Cause?

The financial press is currently fixated on whether U.S. equity markets are in the midst of an AI-driven stock market bubble. With the topic soaking up much of the proverbial oxygen in the room, other important developments in fixed income and money markets are receiving far less attention.

One such development is a burst of unusual volatility in U.S. dollar money markets following the Federal Reserve’s recently completed Quantitative Tightening (QT) program, which significantly reduced aggregate bank reserves. In recent months, repo rate volatility has increased, particularly around month-end reporting periods, and has only been slightly mitigated by the utilization of the Fed’s Standing Repo Facility (SRF). This development harkens back to the onset of the September 2019 repo market disruption, a period marked by sudden funding stress and liquidity shortages—an episode we previously examined in Repo Ruckus Reveals Hidden Issues in Liquidity Markets. The key question for market participants is whether today’s environment could produce a similar outcome—or whether existing liquidity backstops will be sufficient to prevent a repeat of that crisis.

What’s Causing Bank Reserve Levels to Fall?

| Date | Current | September 2019 |

| Reserves | $2.9T | $1.5T |

| Reserves-to-Banking System Assets | 12% | 8% |

| Reserves-to-GDP (as of Q2’25) | 11% | 7% |

Source: Federal Reserve, FRED

Since peaking in December 2021, reserve balances have declined from $4.2 to $2.9 trillion, representing a nearly 30% contraction. While substantial, this decline still leaves the U.S. banking system with higher reserve levels than those in place prior to the 2019 repo market disruption.

Despite appearing safer than 2019 on an absolute basis, current bank reserve levels may still be insufficient due to three key factors:

- Uncertain reserve demand. The amount of reserves banks prefer to hold is difficult to estimate. A Cleveland Fed analysis cites a wide range of estimates for minimum “ample” reserve demand, spanning from $2T to as high as $3.8T. Estimates utilizing direct solicitation of banks have proven unreliable, suggesting that banks themselves don’t fully understand their own reserve needs.

- Dynamic and rising reserve requirements. Reserve demand isn’t static; it scales with balance sheet size and evolves over time. As Bill Nelson, Chief Economist at the Bank Policy Institute notes, the Fed’s current estimate of banks’ reserve demand is three times higher than in 2019 and nearly 100 times greater than in 2008, underscoring how structural changes have reshaped liquidity needs.

- Reserve supply extends beyond Federal Reserve policy. While Fed balance sheet actions are a primary driver, reserve levels are also affected by external factors. For instance, growth in physical cash in circulation reduces reserve balances, all else equal.

Rising Volatility in Money Markets

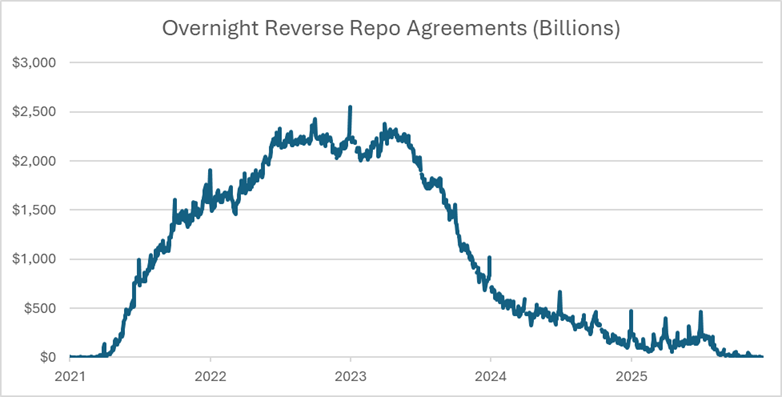

Money market conditions suggest U.S. bank reserves may be approaching an inflection point. Balances in the Fed’s Overnight Reverse Repurchase Agreement (ONRRP) facility, a key contingent source of liquidity for banks and money market funds, have declined from $2T to essentially zero.

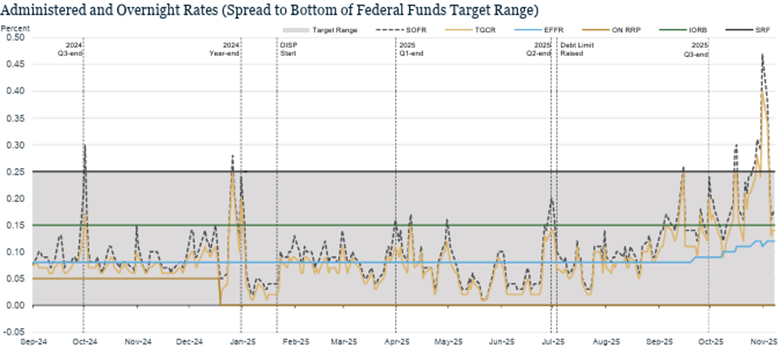

Meanwhile, funding rates are on the rise, signaling increased stress in money markets. The Tri-Party General Collateral Rate (TGCR) and the Secured Overnight Financing Rate (SOFR) have consistently been above the Fed’s Interest on Reserve Balances (IORB), a sign that banks may be increasingly turning to the market to meet reserve needs. During the October and November month-end periods, both TGCR and SOFR temporarily rose above the top end of the federal funds target range.

Source: Robert Perli, Federal Reserve Bank of New York

What Happens When Repo Rates Surge?

The spike in repo rates is problematic for the Fed, as it reduces their control over short-term interest rates that transmit policy decisions to the broader financial markets. The repo market has become an increasingly important source of funding for U.S. Treasury issuance, particularly as hedge funds finance Treasury purchases through short-term repo borrowings.

A severe spike in repo rates could force rapid position unwinds, trigger pockets of dysfunction in the Treasury market, and potentially spill over into broader financial stability risks. In other words, a problem in this niche funding market could quickly become everyone’s problem.

How the Fed is Addressing Repo and Reserve Challenges

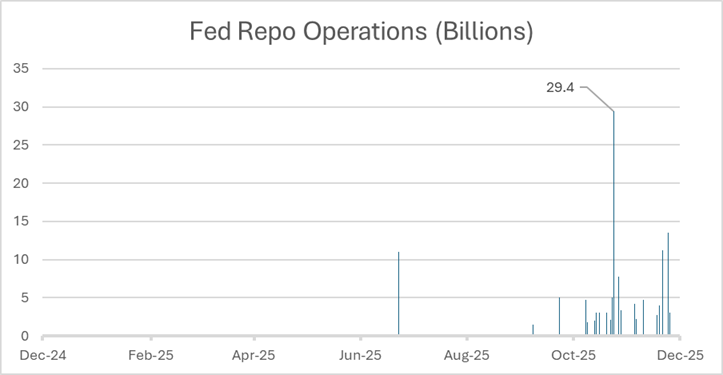

The Fed designed the Standing Repo Facility (SRF) specifically to address this scenario. Established after the 2019 repo market crisis, the SRF allows banks to borrow reserves at the upper bound of the fed funds target range, which currently stands at 3.75% following the Fed’s latest rate decision. In theory, this can act as a reliable liquidity backstop, capping repo spikes by providing banks an alternative to paying high private market rates.

In practice, however, the SRF has fallen short due to underutilization. Bank executives fear that tapping the facility would be perceived by the market as a sign of weakness, akin to using the Fed’s Discount Window. While utilization has increased recently, it remains sporadic and inconsistent.

Source: Federal Reserve Bank of New York, FRED

The Fed is implementing “reserve management purchases” to support liquidity in money markets. Instead of relying on the SRF, the Fed plans to buy Treasury bills in the secondary market with the stated goal of maintaining an “ample” supply of bank reserves. Purchases will begin at $40B a month, with adjustments based on reserve dynamics and market conditions.

This program is expected to ease some of the strain in repo markets as we head into the year-end period. But, the Fed’s endgame remains unclear: is this a temporary fix to smooth short-term volatility, or a material reserve injection? The former provides only temporary relief, while the latter reintroduces balance sheet expansion, which may have efficiency and market distortion costs.

Are Investors Ready for Reserve-Driven Money Market Volatility?

Money markets are flashing warning signals. Scarcity of bank reserves is driving month-end repo rate spikes above the Fed target range, threatening both monetary policy control and Treasury market stability. In response, the Fed is implementing reserve management purchases—$40B monthly in Treasury bills—but whether this represents a temporary bridge or permanent balance sheet expansion remains unclear. Investors and market participants should closely monitor repo market activity over the coming months for signs of stress or disruption.

Key Takeaways

- Reserve Scarcity is Creating Money Market Volatility: The Federal Reserve’s Quantitative Tightening (QT) has resulted in a ~30% contraction in bank reserves, creating potential liquidity shortfalls.

- The Fed’s Grip Over Short-Term Interest Rates Has Loosened: Money market rates are consistently trading above the Fed’s Interest on Reserve Balances (IORB) rate, with temporary spikes exceeding the top of the federal funds target range.

- The Fed Responds with $40B in Monthly Treasury Bill Purchases: To maintain “ample” reserves and ease repo market strain, the Fed has resumed asset purchases, though it’s unclear whether this represents a temporary liquidity measure or a move toward permanent balance sheet expansion.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.