A 10% Credit Card Rate Cap: Relief for Consumers or a Credit Squeeze?

10% Credit Card APR Cap: How It Could Shake Up Banks and Borrowers

Last month, President Trump revived calls for a one-year 10% cap on credit card interest rates to provide financial relief amid an affordability crisis. If passed, this policy would limit the maximum annual percentage rate (APR) that credit card companies can charge to 10%, well below the ~21% national average as of 3Q25.[1] While proposals to cap credit card APRs have circulated in Washington before, the legislative path forward remains unclear.

Policy risk is also broadening beyond a single federal cap. On February 18, Senate Democrats led by Senator Elizabeth Warren floated legislation that would allow states to enforce their own interest-rate limits on national lenders. Warren has also publicly urged JPMorgan CEO Jamie Dimon to support a pilot 10% cap in Massachusetts and Vermont following his comments at Davos about testing the idea.[2]

Despite mounting political pressure and public frustration over high credit card APRs, legislative momentum is murky. The banking industry has resisted strongly against rate caps.[3]

Importantly, credit card usage hasn’t collapsed. Credit performance and transaction volumes have held up. For now, near-term equilibrium appears intact:

- Headline risk persists

- Policy risk remains uncertain

- Issuers continue repricing, tightening, and segmenting where needed

For fixed income and cash investors, the key takeaway is that this is primarily a business-model and earnings issue—not a near-term solvency story for large, diversified banks. The more meaningful risk is second order. If a binding 10% cap were implemented, issuers would likely respond by tightening underwriting standards and restricting access to revolving credit. This may disproportionately affect lower-income and lower-credit-score borrowers—the very group the policy is intended to help.

How Major Banks Could Respond to a Federal Credit Card Rate Cap

Not all financial institutions would be equally affected by a 10% credit card rate cap. The impact would depend primarily on two factors:

- How much of a firm’s business is tied to credit cards

- How effectively the institution can price and manage borrower risk

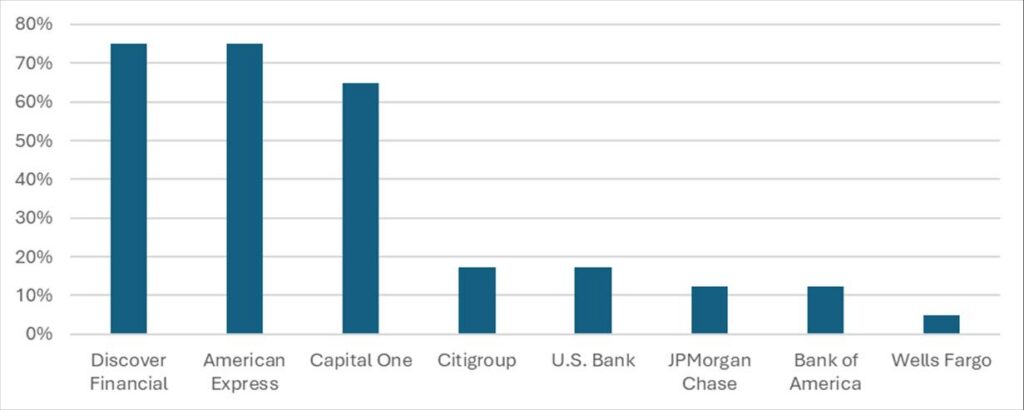

Exhibit 1: Credit card activity as a share of total business (by issuer)

Source: Company filings

Discover, American Express, and Capital One are among the most exposed to a potential 10% credit card interest rate cap because credit cards account for a much larger share of their revenue and earnings model.

At the other end of the spectrum, Wells Fargo has a relatively smaller credit card footprint (in part due to regulatory constraints), which limits its direct earnings exposure.

For the largest U.S. banks, credit cards matter, but aren’t dominant. These institutions benefit from diversified earnings streams across payments, wealth management, commercial banking, corporate banking, and capital markets—alongside substantial capital and liquidity buffers.

Even if an APR cap squeezed credit card yields, large banks could defend profitability through a combination of:

- Repricing other products

- Expense discipline

- Product redesign

- Balance sheet management

What does this mean for fixed income investors?

For investors, the key question isn’t simply: Would this dent a revenue line?

It’s: Would this impair a bank’s capacity to meet obligations while maintaining strong capital and liquidity?

In our view, for global systemically important banks (GSIBs) and other large, diversified institutions, the answer is unlikely.

A binding rate cap may create:

- Modest spread volatility tied to headline/regulatory risk

- Incremental conservatism in underwriting

- A shift toward higher-income borrowers

However, this does not appear to be a near-term solvency story for the largest banks. It’s far more of an equity-earnings and business-model re-optimization issue—unless paired with a broader policy package that simultaneously constrains other revenue streams, such as fees, interchange, or servicing economics.

How Issuers Would Respond: A Predictable, Tried-and-True Playbook

If a 10% credit card cap were imposed in a way that binds, issuers wouldn’t simply accept lower profitability. Instead, they’d likely adjust across multiple economic levers to protect margins and manage risk.

- Tighter underwriting and smaller credit lines: Approvals may shift upward in credit score, income verification standards would tighten, and initial credit lines may get smaller. This is the most direct way to protect economics when yield is capped.

- Greater reliance on fees and back-end pricing: When interest revenue is constrained, pricing pressure tends to migrate into annual fees, late fees (where allowed), balance transfer fees, foreign transaction fees, and other charges. Even when avoidable in theory, these fees often become a bigger burden for less financially flexible households.

- Reduced rewards and fewer cardholder perks: Credit card rewards programs aren’t free—they’re subsidized by interchange income and interest revenue from revolvers. If issuer economics compress, and rewards are trimmed, cash-back percentages may fall, points could devalue, and ancillary benefits may disappear. There’s political irony here: even consumers who pay balances in full may still see the impact through diminished rewards.

- Product simplification: Risk-based pricing supports a wide menu of card products. Interest rate caps can compress that range, pushing the market toward fewer offerings targeted at safer, higher-income customers. Product diversity may decline as risk tolerance narrows.

The common thread across these adjustments is a shift in burden—from high APR to reduced access and less transparent total cost. It’s not likely that demand for credit will vanish, but it may relocate.

Who Bears the Brunt: The Uncomfortable Reality of Credit Card Rate Caps

If there is one takeaway investors should draw from the broader debate over a 10% credit card interest rate cap, it’s this: while rate caps are politically marketed as consumer protection, economically they often function as a gate.

Exhibit 2: balance-carrying behavior by cardholders is highly correlated with credit score, with consumers with lower credit scores more likely to revolve a balance

Source: CFPB[4]

A binding cap pushes lenders to re-examine the borrower pool. The borrowers most likely to be screened out are those with lower credit scores, more volatile income, and less savings—households already operating closest to the edge.

This dynamic is especially important because those same borrowers are the most reliant on revolving credit. As the chart shows, subprime and deep-subprime accounts consistently carry the highest share of balances month to month, while super-prime borrowers are far less likely to revolve. Once mainstream credit tightens, demand doesn’t disappear. Households still face emergencies, medical bills, car repairs, and income gaps between paychecks.

Instead, liquidity needs to shift to alternative products such as:

- Buy-now-pay-later services

- Overdraft programs

- Pawn-style products

- Payday-style products

- Informal credit

These substitutes are often more expensive, less transparent, and less regulated than traditional bank-issued credit cards. The result is a policy that can unintentionally push borrowing costs up for the very group it intends to help.

What Credit Card ABS Tell Us About Rate Cap Risks

In credit card asset-backed securities (ABS), excess spread is the fulcrum. It serves as the trust’s first-loss protection for bondholders and, economically, it is the sponsor’s net interest margin within the trust structure.

In simple terms:

Excess spread = portfolio yield (interest + non-interest income, such as fees and interchange) – credit losses – trust expenses (servicing and bond coupons).

A binding 10% interest rate cap would directly reduce the interest component of yield, and all else equal, compress excess spread. When that buffer erodes far enough, ABS structures are designed to protect bondholders via early amortization[5]. At this stage, the trust stops revolving as planned and shifts to sequential principal paydowns by rating class.

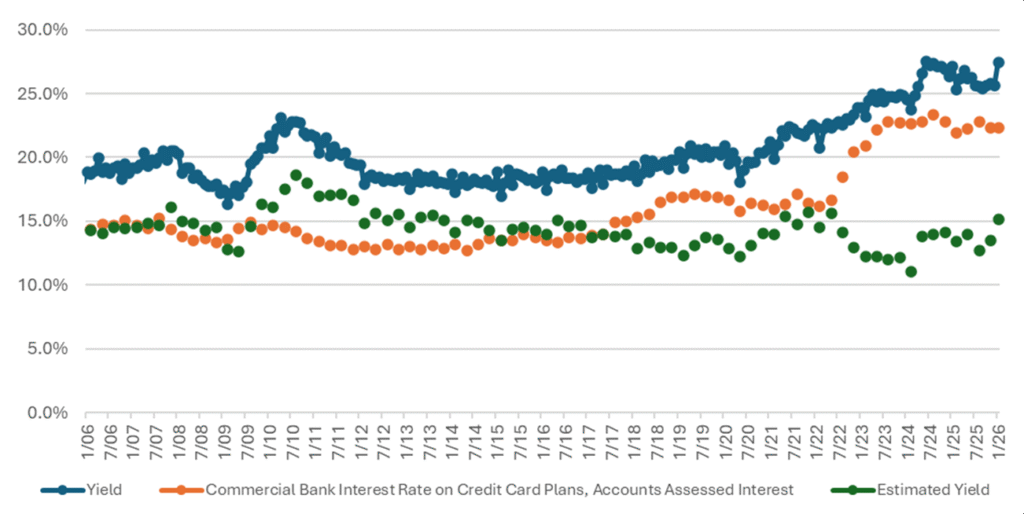

Mechanically, the impact is straightforward: lower yield → lower excess spread, assuming credit losses and trust expenses don’t immediately fall. Based on our estimates, a 10% cap could roughly halve yields for prime credit card ABS — from ~26% to ~13% — and reduce excess spread from ~18% to ~5%.

Exhibit 3: 10% cap estimated impact on credit card ABS yields

Note: ABS disclosures typically do not split yield into interest vs. non-interest components. We use the Fed’s G.19 commercial bank credit card interest rate as a proxy for the interest (APR) portion and assume the remainder of our master trust yield reflects non-interest income (fees/interchange). Under a 10% cap: Estimated Yield = 10% + (Historical Index Yield − G.19 Rate).

Source: Fred, ABS trust metrics

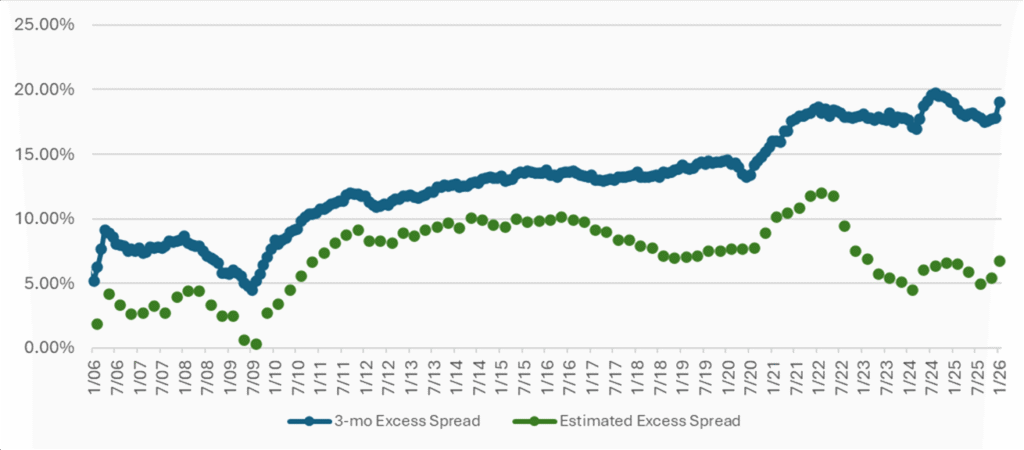

Exhibit 4: 10% cap estimated impact on credit card ABS excess spreads

Note: Estimated Excess Spread = Historical Excess Spread – (Hitorical Yield – Estimated Yield)

Source: Fred, ABS trust metrics

Historically, excess spread dipped below 5% during the 2009 Global Financial Crisis (GFC). At that time, sponsors were generally able to maintain ABS ratings by adding credit enhancement and using tools like discounting receivables to avoid breaching triggers as credit losses spiked.

The key point: 5% is a much thinner cushion than today’s ~18% excess spread. If charge-offs rise meaningfully while interest yield is capped, there is much less room for error in protecting bondholders and maintaining ABS performance.

One nuance worth emphasizing is that issuer behavior matters as much as the cap itself. If a cap forces tighter underwriting, issuers may shrink exposure to higher-loss accounts, which could lower future charge-offs and partially offset yield compression. However, these adjustments could also reshape the receivables pool and trust dynamics, including:

- Seasoning

- Utilization

- Purchase volume

- Payment behavior

It is important to note that this is not our base case, given the uncertain path of implementation. Credit card ABS structures are built to adapt. Sponsors can respond by:

- Tightening credit lines

- Shifting originations up the credit spectrum

- Adjusting pricing and fees where permitted

- Rotating receivables to preserve trust performance

The Bottom Line: A 10% Credit Card APR Cap Could Shrink, Not Boost, Affordability

A 10% credit card interest rate cap, even if revived, is more likely to reshape access to credit than to sustainably lower borrowing costs. The second-order effects are where the real story lies:

- Tighter credit availability for higher-risk borrowers

- Pricing pressure shifting into fees

- Weaker rewards

- A market that favors higher-income customers

From an investor lens, this scenario is unlikely to be materially credit-negative for large, diversified banks. The sharper impact could land on lower-income and lower-credit-score borrowers, who are most likely to lose access to mainstream revolving credit and be pushed toward more expensive alternative credit options.

For credit card ABS investors, the base case remains one of monitoring rather than alarm.

In short, while rate caps are intended to improve affordability, a blunt policy risks delivering the opposite effect: a smaller mainstream credit market and higher borrowing costs in the shadows.

[1] https://fred.stlouisfed.org/series/TERMCBCCALLNS#:~:text=Banking%20%3E%20Consumer%20Credit-,Commercial%20Bank%20Interest%20Rate%20on%20Credit%20Card%20Plans%2C%20All%20Accounts,Release%20Date:%20Mar%206%2C%202026

[2] https://www.bankingdive.com/news/warren-dimon-jpmorgan-credit-card-interest-rate-cap-state-bill/812464/

[3] https://www.wsj.com/finance/banking/the-credit-card-rate-cap-has-stalled-and-issuers-are-doing-just-fine-0694af05

[4] The credit score levels are based on FICO Score 8 and we focus on five credit score levels: Deep subprime (credit score below 580), Subprime (credit scores of 580-619), Near-prime (credit scores of 620-659), Prime (credit scores of 660-719), and Super-prime (credit scores of 720 or above)

[5] For prime bankcard master trusts, a three-month rolling average excess spread below 0% triggers amortization

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.