Investing in AI? The Hidden Risks Behind the Hype

Nearly four years after we first highlighted the credit advantages of Big Tech’s large cash holdings, balance sheet strength has only grown more important. The rapid adoption of generative AI is driving a surge in infrastructure and data-center spending, and capital expenditures (capex) that were once modest are now among the largest uses of corporate cash—and one of the biggest sources of financial risk.

Exhibit 1: Capital expenditures for five largest hyperscalers

Source: Company 10-K and 10-Q filings

While investors were previously accommodative of these investments due to insatiable demand and attractive growth opportunities, they have become increasingly scrutinous. Concerns about generating sufficient return on investment (ROI) and the growing complexity of AI financing structures (including circular deals among major technology platforms) have contributed to equity market volatility and recurring “AI bubble” headlines.

In short, investors may no longer be content with the promise of growth at any cost.

Separating Hype from Credit Risk

Whether we are in an AI bubble is impossible to know in real time, but investors should not be spooked by headlines. A high-growth startup with significant cash burn does not typically face the same risks as a large, profitable company with a robust balance sheet.

Ultimately, investors evaluating the debt of issuers funding AI infrastructure should stay focused on the fundamentals and be selective about which opportunities belong in their portfolios.

Investing in AI-Driven Debt: Key Investor Considerations

1. Debt and Off-Balance Sheet Financing

Hyperscalers have been tapping the fixed income markets to fund unprecedented levels of AI-driven capital investment.

- BNY Mellon noted that hyperscalers issued $121 billion in 2025.[1]

- J.P. Morgan expects significant issuance in 2026, largely driven by AI investment needs.[2]

Companies have also increasingly used operating and financing leases for equipment, which may reduce up-front cash outlays and provide greater flexibility compared with purchasing assets outright with debt financing. Private credit has also become a growing source of funding, as we discussed in our whitepaper, “Key Themes Investors Shouldn’t Ignore in 2026.”

Rising Use of Complex Structures

Companies are increasingly turning to complex funding structures, such as joint ventures, to keep financing off the balance sheet and reduce reported borrowing.

The most high-profile example is Meta’s $27 billion joint venture with Blue Owl to develop the Hyperion data center. While these arrangements can lower up-front capital costs, they often lock companies into long-dated payment obligations and may increase exposure to changing market conditions.

In Hyperion’s case, a 16-year residual value guarantee creates the potential for a material liability if Meta terminates the agreement early—risk that’s difficult to quantify as it depends on future asset values, utilization, and contract terms.

The Leverage Risks Investors Can’t Ignore

When assessing an issuer’s leverage, investors should look beyond reported debt and incorporate off-balance-sheet commitments—including leases, joint ventures, guarantees, and other contractual obligations—into their analysis.

Investors should also evaluate a company’s cash holdings, as strong liquidity may offset net debt and ease leverage burdens.

Exhibit 2: Cash and cash equivalents relative to total debt and operating leases of the five largest hyperscalers

Source: Company filings as of 9/30/25 (for Oracle, as of 11/30/25)

2. Cash Flow Generation

Strong cash flows are important to credit quality for obvious reasons: companies need to fund ongoing operations, invest in growth, and meet contractual obligations.

For AI-focused issuers, free cash flow (FCF) is especially important because it captures the real cost of today’s data-center and infrastructure build-out by subtracting capital expenditures.

This explains why accounting profits may rise even as FCF declines—a pattern that has become increasingly visible among hyperscalers.

Exhibit 3: On aggregate, free cash flow has decreased for 5 largest hyperscalers while net income has increased

| Trailing Twelve Months (TTM)** | Versus: Year-Ago Period | % Change Year-over-Year | |

| Free Cash Flow* | $191,726 | $231,614 | -17% |

| Net Income | $379,598 | $301,813 | +26% |

*Free cash flow is defined as cash from operating activities minus capital expenditures and principal repayment of finance leases

**Data calculated from latest available figures as of 1/15/2026

Source: Company 10-K and 10-Q filings

Why Free Cash Flow Matters

FCF pressure has been broad-based, but companies that maintain positive FCF may be better positioned to:

- Absorb capex volatility

- Continue investing

- Avoid leaning on external financing

Unsurprisingly, higher-rated issuers have been able to keep cash flow positive, giving them breathing room to continue AI and infrastructure investments, while lower-rated firms have reported meaningfully negative FCF.

Strong liquidity positions also provide important flexibility, as ample cash and short-term assets can reduce credit risk if FCF turns negative for a period. Of greater concern are companies that may have:

- Persistently negative FCF

- Weak liquidity

- Increased dependence on external funding

These conditions increase the riskiness of their debt, especially if market conditions tighten or growth expectations reset.

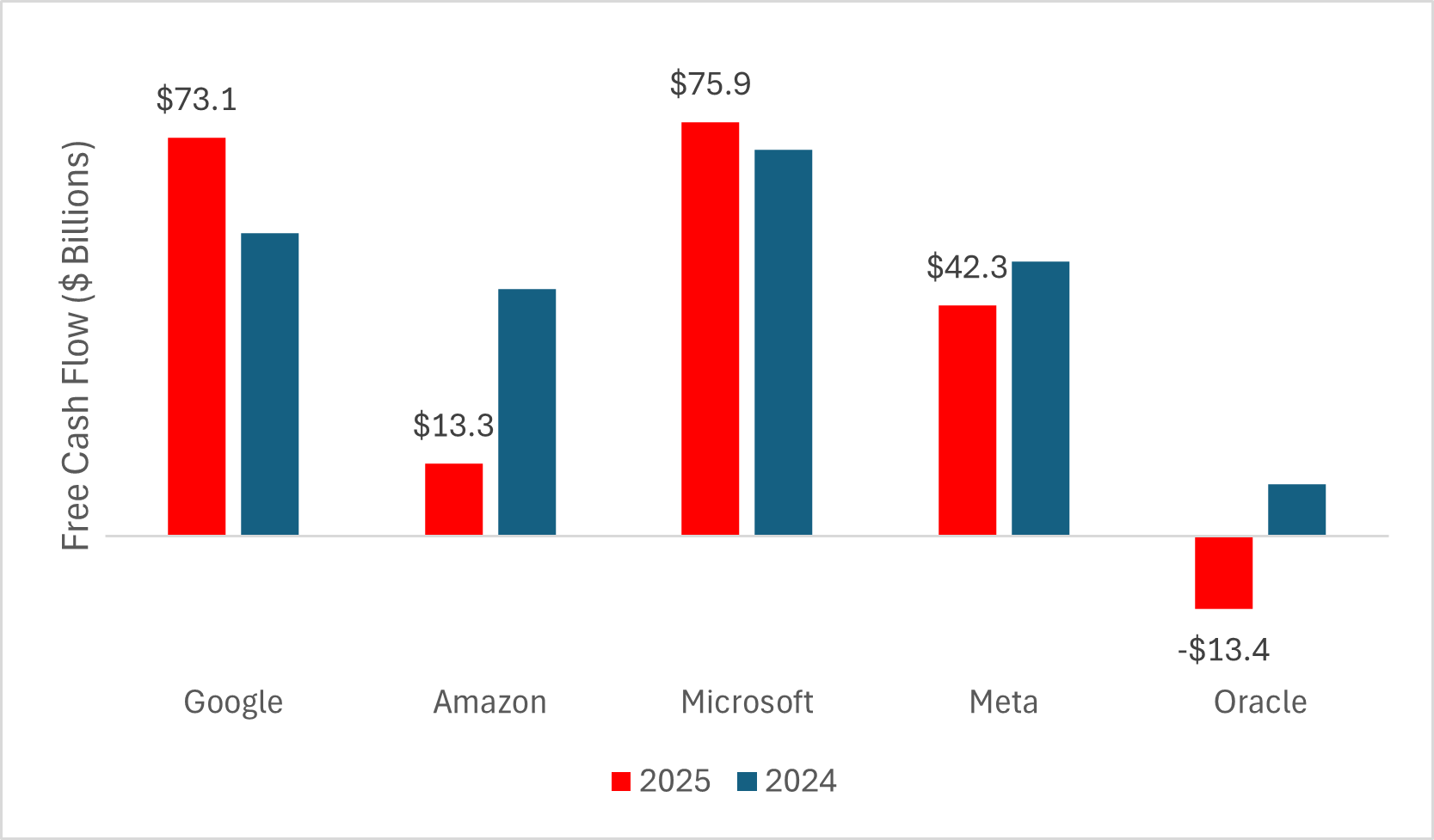

Exhibit 4: Free cash flow generation remains positive for most hyperscalers despite capital intensity

Source: Company 10-K and 10-Q filings

Investor Takeaway

Cash investors evaluating hyperscalers should focus on companies with:

- Strong, positive FCF

- Manageable capital intensity

- Limited cash-flow deficits

Companies with robust FCF typically have greater flexibility to withstand periods of pressure, but investors should reassess exposure if FCF becomes persistently compressed or turns negative.

3. Revenue Diversification

Business mix matters. Companies with diversified revenue streams tend to be more resilient than those heavily concentrated in AI-related segments.

For instance, semiconductor manufacturers like Nvidia have experienced meteoric revenue growth in recent years due to high demand for their products, but the share of AI-semiconductor offerings relative to the company’s total revenues amplifies the risk of a potential downturn.

In contrast, the three largest hyperscalers—Amazon, Microsoft, and Alphabet—benefit from meaningful diversification beyond cloud infrastructure. While parts of their businesses remain cyclical, a broader revenue base may soften the impact of a slowdown in any single segment.

The Investor’s Checklist for AI Debt

In the ongoing infrastructure arms race, investors looking to purchase debt from AI-focused companies should ask the following questions:

- Are the company’s debt levels and off-balance sheet financing supported by revenue and earnings growth?

- Is the company’s cash flow generation sufficient to fund sizable capital investments?

- Does the company have strong liquidity?

- Can the company’s revenue streams withstand a downturn in AI demand without substantially weakening credit quality?

Bottom line:

Companies with low leverage, positive free cash flow, and diversified revenue streams tend to represent safer investment opportunities than firms with weaker balance sheets and more volatile growth profiles.

[1] BNY Mellon – Record-Breaking AI-Related Debt Issuance in 2025

[2] JP Morgan – US High Grade Credit 2026 Outlook

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.