New Vice Chair for Supervision Michelle Bowman and the New Deregulatory Wave: Implications for U.S. Banks

Michelle “Miki” Bowman’s nomination as the Federal Reserve’s Vice Chair for Supervision was confirmed by the U.S. Senate on June 4th, 2025[1]. The confirmation aligns with Washington’s broader effort to unwind regulatory safeguards implemented after the Global Financial Crisis. During her testimony in April, Bowman advocated for “pragmatic tailoring”, adjusting capital buffers, accelerating merger approvals, easing consumer protection rules, and consolidating bank supervisory agencies[2]. These priorities are in-line with the White House, Treasury, and other banking agency heads. Such changes promise near-term profitability and flexibility for banks, but raise concerns regarding capital adequacy, supervisory independence, and the long-term regulatory framework.

Capital, SLR/GSIB surcharge, and liquidity

The core of the deregulatory agenda centers around revising the Basel III Endgame proposal to be capital-neutral, significantly paring back the currently proposed requirements. The original 2023 draft, which would have raised common-equity requirements by 19% at the eight U.S. global systemically important banks (GSIBs) and by about 16% across all large banks, is likely to be pared back dramatically[3]. Bowman voted against the 2023 draft, arguing there was “insufficient evidence” to justify its costs and warning that pushing large-bank standards onto smaller lenders could result in “harmful, unintended consequences.”[4] Regulators now aim to reduce operational-risk add-ons, moderate market-risk weights on Treasury repo and agency mortgage-backed securities (MBS), and recalibrate credit-valuation charges. This aligns with Bowman’s earlier calls for “granular changes that will improve the effectiveness and efficiency of the rule.”[5]

In addition, both the Treasury Secretary and Bowman have called for reforms to reduce capital buffers. The Fed has recently announced efforts to enhance the transparency of stress tests and to smooth their impact on bank capital requirements. Additionally, the Fed has floated a rule that would average CCAR (Comprehensive Capital Analysis and Review) results over two years and publish more model details. Bowman first advocated for these reforms in a 2024 speech aiming to curb “volatility in firm results from year to year,” tighten the link between hypothetical stress scenarios and the stress-capital buffer, and remedy the “broad lack of transparency” that clouds current stress tests[6]. According to Fed staff, applying averaging since 2019 would have lowered the industry’s stress capital buffer by roughly 17%, allowing banks to operate with smaller management cushions[7].

Exhibit 1: Actual vs 2-Year Average Stress Capital Buffer of the 8 U.S. GSIBs

| Banks | Actual Stress Capital Buffer | 2-Year Avg. Stress Capital Buffer | ||

| 2023 | 2024 | 2023 | 2024 | |

| BAC | 2.5 | 3.2 | 3.0 | 2.9 |

| BK | 2.5 | 2.5 | 2.5 | 2.5 |

| C | 4.3 | 4.1 | 4.2 | 4.2 |

| GS | 5.5 | 6.2 | 5.9 | 5.9 |

| JPM | 2.9 | 3.3 | 3.5 | 3.1 |

| MS | 5.4 | 6.0 | 5.6 | 5.7 |

| STT | 2.5 | 2.5 | 2.5 | 2.5 |

| WFC | 2.9 | 3.8 | 3.1 | 3.4 |

Source: BAC, BK, C, GS, JPM, MS, STT, WFC

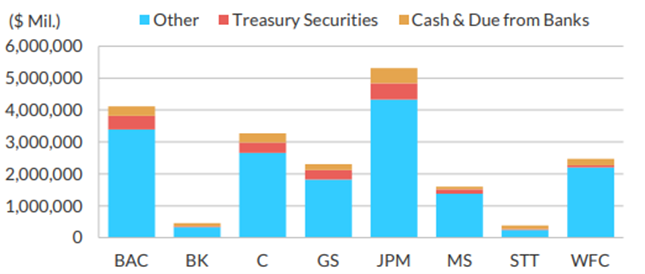

Bowman has also signaled her intent to improve liquidity in the Treasury market, implying a regulatory change to the Supplementary Leverage Ratio and the GSIB surcharge for the largest banks. She is considering excluding reserve balances and Treasuries from the SLR to ensure that “primary dealers have adequate balance-sheet capacity to intermediate Treasury markets.”[8] Across the eight U.S. GSIBs, removing those “risk-free” assets could lift reported SLRs by more than 100 basis points on average and lower the GSIB surcharge. This move could help level the playing field among GSIBs (cash is already exempt for BNY Mellon and State Street); however, relaxing both risk-weight and leverage constraints at once may weaken the redundancy built into the post-crisis framework. Therefore, Bowman suggests a “targeted approach” to liquidity reform. Addressing lessons from the 2023 banking stress, Bowman cautions that the impulse to “do something” can lead to overshoot, and instead advocates for incremental steps to strengthen bank balance sheets.[9]

Exhibit 2: Composition of SLR Denominator at 4Q24 (exclusion of treasuries, cash suggest moderate relief)

Source: Fitch Ratings, BAC, BK, C, GS, JPM, MS, STT, WFC, FR Y-9C

Accelerating Bank M&As

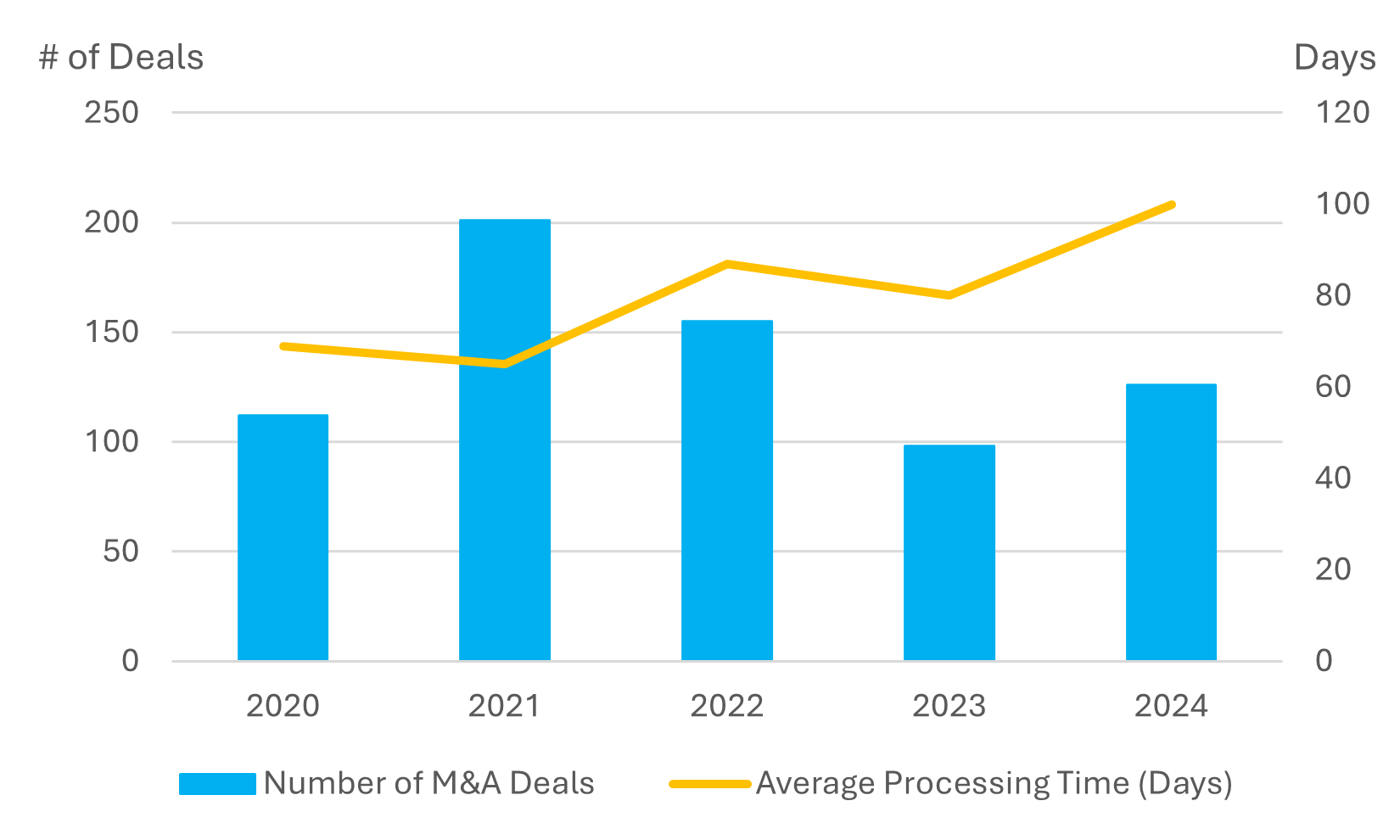

In parallel with capital reforms, regulators are also turning their attention to streamlining bank mergers. Bowman has called for regulators to adopt a 180-day statutory decision clock for merger applications, arguing that year-long reviews “impose unnecessary costs” and leave management teams in limbo[10]. This stance complements the FDIC’s recent policy reversal in March 2024, when they withdrew the 2024 policy statement on state-bank mergers and scrapped stringent criteria that had lengthened reviews[11]. Acting FDIC chair Travis Hill has since remarked on pending initiatives to encourage de novo bank formation, including a simplified application process, lower standards for community banks in underserved areas, and encouragement of nontraditional charters, such as for industrial loan companies[12].

Exhibit 3: M&A deals are taking longer to approve

Source: S&P Global and Federal Reserve

The Office of the Comptroller of the Currency (OCC) is moving in the same direction. Acting Comptroller Rodney Hood has echoed Bowman’s call for faster approvals of bank mergers and new charters, emphasizing that lengthy regulatory reviews deter new entrants at a time when shifting technology and demographics make innovation in banking more necessary than ever[13].

From a credit-risk standpoint, the policy shift is constructive. Faster, rule-based merger reviews could help mitigate uncertainty, improve synergy realization, and ultimately strengthen credit quality, especially for small to midsize banks.

Consumer-protection rollbacks and the outlook for fee income

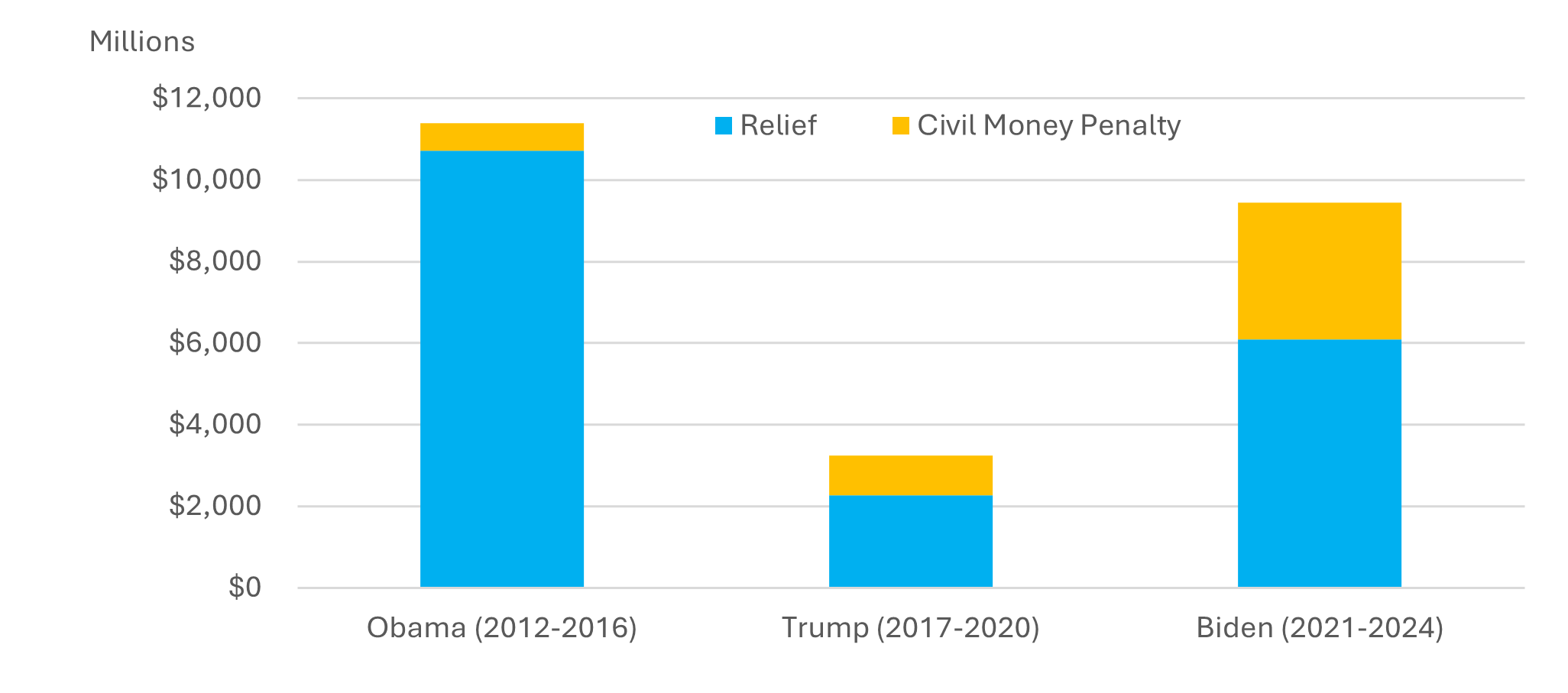

The Consumer Financial Protection Bureau (CFPB) has undergone one of the most dramatic regulatory shifts between administrations in recent history. Under the Biden administration, banks faced mounting pressure on noninterest income from proposed caps on overdraft fees, credit card late fees, and debit card interchange rates.

Exhibit 4: Penalties and Consumer Compensation under Previous Administrations

Source: CFPB

That direction has now reversed. The CFPB, under new leadership, has suspended enforcement of small-dollar lending rules, halted rulemaking on “buy now, pay later” products, and withdrawn support for fee caps[14]. In April 2025, Congress overturned the CFPB’s overdraft fee rule and its expanded oversight of digital wallets. Michelle Bowman is expected to reinforce this deregulatory agenda. She has opposed the Fed’s proposed cap on debit interchange fees, arguing the disproportionate burden on smaller banks and potential disincentives for fraud prevention and card issuance[15]. Her appointment would likely solidify the rollback of prior consumer protection measures and eliminate new restrictions on fee income.

While this shift supports earnings and revenue diversification, it also raises the risk that banks could overreach. A more permissive regulatory environment may increase operational and reputational risk, particularly if consumer protection standards weaken.

Consolidating agencies, centralizing power

Amid broader deregulatory trends, there is momentum towards centralizing regulatory oversight, driven partly by a February 2025 executive order mandating the Office of Management and Budget review of regulations from the Fed, OCC, and FDIC[16]. Bowman has echoed concerns about the complexity and overlap of the current system, stating in her confirmation hearing that “the U.S. regulatory framework has grown expansively to become overly complicated and redundant, with conflicting and overlapping requirements.”[17] She emphasized the need for “pragmatic” regulation that is efficient, risk-focused, and avoids imposing unnecessary costs on banks or consumers. However, centralizing authority under one regulator risks politicizing supervision, potentially weakening agency independence and long-term regulatory credibility.

Credit Outlook

In the short term, deregulatory measures support earnings without immediately affecting credit ratings, as banks maintain strong capital positions. However, long-term credit profiles may face pressure if reduced capital buffers and increased risk appetites coincide with economic deterioration. Weakened supervisory independence could further complicate future crisis management.

Following Bowman’s recent confirmation, the aforementioned policy changes may soon take effect. The regulatory pendulum has swung toward deregulation. Whether this shift ultimately boosts sustainable returns or plants the seeds of the next stress episode will depend on how banks and their supervisors balance increased flexibility with enduring prudential safeguards.

[1] Reuters – Fed’s Bowman confirmed by Senate to central bank’s top regulatory post

[2] The Federal Reserve – Governor Michelle W. Bowman Nomination Hearing

[3] Federal Register – Regulatory Capital Rule: Large Banking Organizations and Banking Organizations With Significant Trading Activity

[4] The Federal Reserve – Statement by Governor Michelle W. Bowman on Proposed Rules to Strengthen Capital Requirements for Large Banks

[5] The Federal Reserve – Perspectives on U.S. Monetary Policy and Bank Capital Reform by Michelle W. Bowman

[6] The Federal Reserve – The Future of Stress Testing and the Stress Capital Buffer Framework

[7] The Federal Reserve – Proposed rule to reduce the volatility of the stress capital buffer requirement

[8] The Federal Reserve – Bank Regulation in 2025 and Beyond

[9] The Federal Reserve – Bank Liquidity, Regulation, and the Fed’s Role as Lender of Last Resort

[10] The Federal Reserve – Bank Mergers and Acquisitions, and De Novo Bank Formation: Implications for the Future of the Banking System.

[11]FDIC – FDIC Statement of Policy on Bank Merger Transactions

[12] FDIC – Update on Key Policy Issues

[13] ABA Banking Journal – Acting OCC head discusses regulatory tailoring, bank merger reviews

[14] CFPB – CFPB Announcement Regarding Enforcement Actions Related to Buy Now, Pay Later Loans

[15] The Federal Reserve – Statement on Proposed Revisions to Regulation II’s Interchange Fee Cap by Governor Michelle W. Bowman

[16] The White House – Ensuring Accountability for All Agencies

[17] The Federal Reserve – Governor Michelle W. Bowman Nomination Hearing

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.