Privatizing America’s Housing Giants: How Fannie Mae and Freddie Mac Could Reshape Bond Markets for Investors

Introduction: Why GSE Privatization Matters to Investors

Given their oversized role in home mortgages, any discussion of Fannie Mae and Freddie Mac’s potential privatization tends to capture investors’ attention. Recent developments suggest that the Trump administration is exploring plans to sell the government’s stakes in the government-sponsored enterprises (GSEs) through an initial public offering (IPO) as early as the end of 2025. A lot remains unknown as to whether the government will keep the firms in conservatorship, revise the preferred stock purchase agreements, or sever its ties altogether by requesting Congress to end their GSE charters.[1]

Unlike gleeful hedge fund managers who scooped up the firms’ nearly worthless shares in hopes of a big payday, the sentiment among fixed income investors is guarded – if not alarmed. Since the government’s takeover during the 2008 Great Financial Crisis (GFC), and for decades before that, Fannie Mae and Freddie Mac debt has been viewed as nearly as creditworthy as U.S. Treasury securities, thanks to implicit government guarantees and their conservatorship status. Any policy that significantly weakens investor confidence may result in higher borrowing costs for mortgage borrowers, increased market volatility, and elevated credit risk for bond investors.

In this white paper, we will explain why full privatization of Fannie Mae and Freddie Mac remains unlikely in the foreseeable future. Institutional liquidity investors of GSE bonds and discount notes remain relatively insulated from market chatter thanks to the short maturities of their holdings and the likely grandfathered status of outstanding GSE debt, should Congress move to end the housing GSE charters – an outcome widely viewed as politically unpopular in Washington.

Fannie Mae and Freddie Mac: Core Players Shaping U.S. Mortgage and Housing Finance

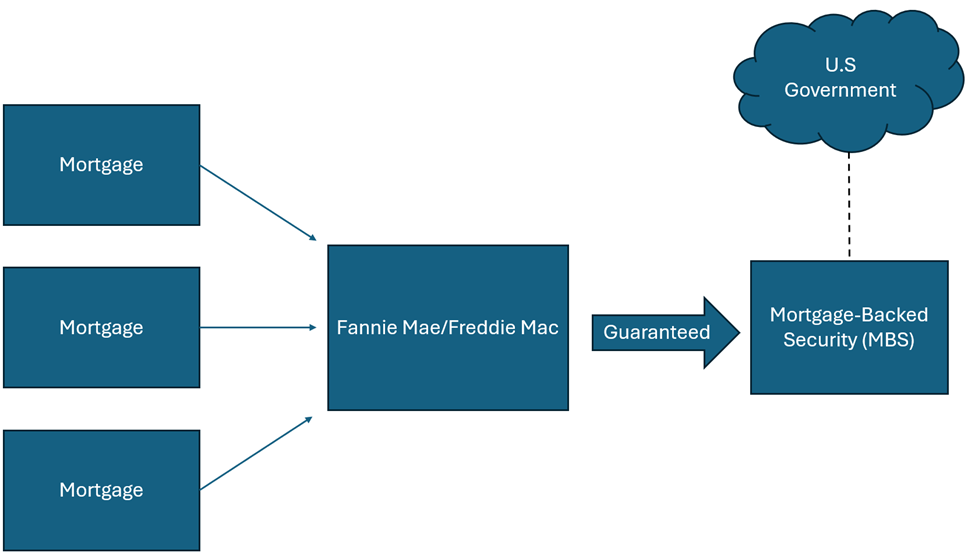

The Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac) are federally chartered corporations known as government-sponsored enterprises (GSEs) that play an important role in the U.S. housing finance system. These institutions purchase mortgages from lenders and either hold them in a portfolio or package them into mortgage-backed securities (MBS) with credit guarantees for sale to investors.

Fannie Mae was established in 1938 as part of the New Deal to provide mortgage market liquidity during the Great Depression, while Freddie Mac was created in 1970 to expand the secondary market and compete with Fannie. Today, both firms are regulated and supervised by the Federal Housing Finance Agency (FHFA) – an independent agency established by the Housing and Economic Recovery Act of 2008 following the Global Financial Crisis (GFC). The U.S. Treasury Department holds preferred shares and warrants in both entities, while common shares, though still in existence, were severely diluted and deemed virtually worthless in 2008 when the government placed the firms under conservatorship.

As primary housing GSEs, Fannie Mae and Freddie Mac enjoy certain federal privileges, including exemptions from certain taxes and securities regulations, in exchange for fulfilling their public policy mission of supporting mortgage market liquidity and affordability. Their core functions include purchasing conforming mortgages that meet specific criteria (like loan size and borrower credit), securitizing them into agency MBS, and guaranteeing principal and interest payments to investors. This process provides liquidity to lenders, keeps mortgage rates low, and promotes affordable homeownership.

Exhibit 1: A Visual Guide to MBS Securitization by Fannie Mae and Freddie Mac

The GSEs importance to the U.S. economy cannot be overstated. By providing capital to the housing market, they sustain economic growth, job creation in construction, and wealth building through homeownership. According to the latest company filings, Fannie Mae and Freddie Mac collectively guarantee $7.6 trillion in home mortgages, representing about 59% of total mortgage balances nationwide.[2]

From Implicit Guarantee to Conservatorship: Inside the Senior Preferred Stock Purchase Agreements

Before the 2008 Global Financial Crisis (GFC), investors widely believed that the U.S. government would step in and honor debt issued by Fannie Mae and Freddie Mac – a phenomenon known as implicit guarantee. This assumption allowed both government-sponsored enterprises (GSEs) to borrow at near-Treasury rates, which fueled growth but also encouraged risk-taking. According to a Federal Reserve Bank of New York paper, implicit government backing accounted for more than half of the firms’ stock valuation, while guaranteed GSE mortgage rates were approximately seven basis points lower than comparable primary mortgage rates.[3]

The combination of this implicit guarantee and the GSEs’ public policy role in housing finance led major credit rating agencies – including Moody’s, Standard & Poor’s, and Fitch Ratings – to receive the same credit ratings as U.S. Treasury securities, reinforcing investor confidence in agency debt. This perceived backing remains a defining characteristic of GSE bonds today.

The subprime mortgage crisis that triggered the 2008 financial collapse led to the government’s intervention and the placement of both firms into federal conservatorship under the U.S. Treasury and the Federal Housing Finance Agency (FHFA). The Housing and Economic Recovery Act of 2008 (HERA), which established the FHFA, set forth a set of conservatorship goals, including preservation of the GSE’s assets and the eventual return to sound financial condition. Under conservatorship, control of corporate governance and board appointments shifted from common shareholders to the FHFA.[4] This move did not weaken but rather strengthened the implicit guarantee GSE-issued bonds.

HERA also authorized the creation of Senior Preferred Stock Purchase Agreements (PSPAs), between the FHFA and the U.S. Treasury to ensure adequate funding for both GSEs. Amended in 2008, 2009, 2012 and 2021, the PSPAs provided up to $200 billion (later adjusted to formulaic commitments) in capital support to each GSE. Over time, Fannie Mae and Freddie Mac withdrew $119.8 billion and $71.7 billion, respectively. In return, the Treasury received $1 billion of senior preferred stock in each GSE, along with warrants to purchase 79.9% of common shares at no cost. The GSEs agreed to make a quarterly dividend on these senior claims – known as “liquidation preference.”

A key amendment in 2021 allowed both GSEs to retain earnings as capital reserves until they meet the regulatory minimum capital requirements.[5] At the end of the 2024 fiscal year (September 30, 2024), the combined cumulative liquidation preference totaled $334 billion, while the remaining Treasury funding commitment was $254.1 billion. Collectively, the GSEs’ net worth increased to $147 billion, still below the minimum regulatory capital framework requirements of 2.5% of tier 1 capital, which translates into $187 billion for Fannie Mae and $141 Billion for Freddie Mac, totaling $328 billion.

The latest U.S. Treasury’s Financial Report of the United States Government notes that “to date, Congress has not passed legislation nor has FHFA taken action to end the GSEs’ conservatorships. The GSEs continue to operate under the direction of FHFA as conservator.”[6] This maintains their critical role in housing finance, credit markets, and mortgage-backed securities (MBS) in issuance.

Why Is Privatization a Hot Topic Now?

The renewed discussion around privatizing Fannie Mae and Freddie Mac reflects both policy momentum and market speculation about the future of U.S. housing finance, capital markets, and government-sponsored enterprises (GSEs). During the first Trump administration, the White House and the U.S. Treasury Department took steps to move the GSEs out of federal conservatorship toward eventual re-privatization – a policy that remains central to today’s financial and political debate:

- Policy Direction Set by Treasury: In March 2019, President Trump issued a Memorandum on Federal Housing Finance Reform, directing the Treasury Department and the Department of Housing and Urban Development (HUD) to develop a plan for ending the GSEs’ conservatorships and reducing federal risk in housing finance.[7] In September 2019, the Treasury released its Housing Reform Plan, calling for recapitalizing Fannie Mae and Freddie Mac, ending the “net worth sweep,” and allowing firms to rebuild capital as a step toward eventual exit from conservatorship.[8]

- Capital Retention Agreements: The Housing Reform Plan also allowed Fannie Mae to retain up to $25 billion as capital and Freddie Mac up to $20 billion. In January 2021, shortly before Trump left office, the Treasury and FHFA amended these agreements to raise the capital retention levels significantly, allowing the GSEs to build cushions against future risk.[9]

- Regulatory Actions under FHFA Director Mark Calabria: As FHFA Director, economist Mark Calabria was a strong proponent for reducing government involvement in the GSEs and restoring them to private ownership. He issued the Enterprise Regulatory Capital Framework (ERCF) – a set of bank-like capital requirements designed for the GSEs as a precondition for release from conservatorship. The ERCF sought to align risk management, guarantee fee pricing, and capital standards with those expected of private financial institutions.[10]

Despite these efforts, full privatization did not occur during the first Trump term due to an estimated capital shortfall of several hundred billion dollars, limited congressional consensus on housing finance reform, and investor concerns about the potential impact on mortgage rates and market stability if privatization moved too quickly.

Since resuming office in January 2025, the second Trump administration has revived the privatization efforts:

- Initial Public Offering (IPO): The administration is reportedly considering a public offering of 5-15% of Fannie Mae and Freddie Mac shares, potentially raising $30 billion in equity capital and valuing the combined entities between $500 and $700 billion.[11] Such a move would mark their return to major stock exchanges for the first time since 2010 and may reshape GSE equity markets.

- Ending Conservatorship: The move is part of a broader effort to end the federal conservatorship.

- Government Guarantee: The plan includes maintaining either an “implicit” or “explicit” government guarantee even after the IPO. President Trump has publicly reaffirmed that the U.S. government will retain its oversight role, as well as its “implicit GUARANTEEs.”[12]

- Pulte’s Role: Bill Pulte, the current FHFA Director, has been a vocal supporter of the privatization agenda by publicly echoing the president’s call to end government oversight. He raised the possibility of a merger between Fannie Mae and Freddie Mac, into a single entity he called “The Great American Mortgage Corporation.”[13]

- Meeting with Banks: Reports indicate that President Trump and his administration have engaged with top Wall Street bank executives to discuss potential IPO structures and methods for bringing the GSEs back to public markets.[14]

Hedge funds are also keen on privatization because they hold junior preferred and common shares purchased cheaply during the rubble of the financial crisis, potentially yielding billions in windfalls if the firms’ shares surge post-IPO. Notably, Pershing Square’s founder and activist investor Bill Ackman has long maintained significant positions in Fannie Mae and Freddie Mae, with investments estimated to be worth as much as $10 billion.[15]

Main Obstacles to Fannie Mae and Freddie Mac Privatization

Despite President Trump and FHAF Director Bill Pulte’s public support, the path to a full privatization of Fannie Mae and Freddie Mac will likely be a long and complex one. Several major financial, regulatory, and political barriers continue to impede progress toward removing the government-sponsored enterprises (GSEs) from federal conservatorship and restoring them as fully independent, market-driven entities within the U.S. housing finance system.

Regulatory Capital Shortfall: Under the Enterprise Regulatory Capital Framework (ERCF) introduced by former FHFA Director Mark Calabria, Fannie Mae and Freddie Mac currently face a combined regulatory capital shortfall of $181 billion, representing a $328 billion capital requirement offset by $147 billion of retained earnings as of late 2024.[16] With annual combined net income of $29 billion, it would take at least seven years for the GSEs to build sufficient capital organically to meet the minimum capitalization standards for privatization.[17] The rumored $30 billion IPOs would only cover a small fraction of the sum and, if press reports are to be believed, proceeds could flow to the U.S. Treasury’s coffers, rather than directly to the GSEs. For context, CoreWeave, a Nvidia-backed cloud computing platform, raised $1.5 billion in its March 2025 IPO, marking the largest public offering so far this year. It is doubtful that Fannie Mae and Freddie Mac could raise nearly 100 times as much cash as CoreWeave did in one fell swoop.[18]

Treasury’s Liquidation Preference: Another major obstacle is the U.S. Treasury’s $334 billion senior preferred shares, known as “liquidation preference,” which continues to grow as capitalized dividends with recent amendments to the preferred stock purchase agreement. Unless the Treasury decides, on behalf of federal taxpayers, to give the GSEs a generous gift by forgiving its preferred stakes, Fannie Mae and Freddie Mac will likely continue to be under government control. Given the current political climate, it appears unlikely that policymakers would part ways with such a large government asset – particularly $300+ billion – so that hedge fund managers can reap a windfall from GSE privatizations.

Market Implications: A third obstacle lies in addressing market implications from the perceived loss of implicit government guarantee. Despite President Trump’s sound bite, ending conservatorship could generate uncertainty about the continued backing of the GSEs, leading to potential rating downgrades, especially during a market downturn.

Congress’ Role & Timeline: Finally, Congress plays a key role in shaping the regulatory framework governing the GSEs. Any move toward privatization would likely require new legislation addressing explicit guarantees, regulatory reforms, and potentially the termination of GSE charters. One such proposal, H.R. 1209 – The End of GSE Conservatorship Preparation Act of 2025, directs the U.S. Treasury to present Congress completed proposals for ending the conservatorships.[19] Given the divided political environment and competing priorities, however, the timeline for any legislative action remains highly uncertain.

Why Bond Investors Are Watching GSE Privatization

Fixed-income investors, particularly those holding agency bonds and mortgage-backed securities (MBS) issued by Fannie Mae and Freddie Mac, are keenly interested and understandably nervous about the ongoing privatization talks. Investors tend to like “agency” debt issued by Fannie/Freddie, as well as mortgaged-backed securities (MBS) guaranteed by the GSEs. These instruments are highly attractive due to their strong market liquidity, low default risk, and yields slightly above U.S. Treasuries.

Supporters of GSE privatization, including President Trump and Director Pulte, argue that full privatization of the GSEs would reduce taxpayer exposure, create potential for housing finance innovation, and higher income potential for risk-tolerant investors. However, many in the bond market worry that a rushed move may lead to elevated credit risk, disrupt the agency MBS market, and drive higher mortgage rates for homeowners. If privatized, credit ratings on the GSEs’ debt may drop, resulting in bond value losses and reduced market liquidity, especially if government backing is removed.

Moreover, critics further warn of a “moral hazard” reminiscent of the 2008 financial crisis. Should the U.S. government maintain guarantees for privately held GSEs, it could incentivize riskier lending practices. Conversely, if the government openly abandons its prior practice of implicit guarantee, investor confidence could quickly diminish, threatening the GSEs’ ability to fund mortgage guarantees through private markets – potentially forcing a return to conservatorship.

Conclusion: Key Takeaways for Investors on GSE Privatization

The privatization of Fannie Mae and Freddie Mac represents a complex and potentially transformative shift for the U.S. housing finance system and bond markets. For bond investors, several key issues emerge:

- Credit Assurance: Will the implicit government guarantees remain, or could the removal of federal backing increase credit risk for agency bonds and GSE debt?

- Market Stability: Mismanaged privatization could disrupt secondary mortgage markets, reduce agency MBS liquidity, drive up mortgage rates, and impact broader financial system stability.

- Alignment of Interests: Different stakeholders hold divergent priorities. Understanding these tension points is crucial for informed investment decisions.

- Yield Opportunities: Privatization may offer higher yield opportunities for risk-tolerant investors — but only if risk is priced in.

- Timeline Considerations: The potential impact on institutional liquidity investors hinges on the timing of resolving each of the key barriers, including capital shortfalls, Treasury liquidation preference, and regulatory reforms, to privatization.

In the final analysis, the path to full GSE privatization may be a multi-year process requiring capital restructuring, regulatory clarity, and legislative action. Investors in Fannie Mae and Freddie Mac bonds should carefully monitor policy developments, market liquidity, and credit rating trends as these enterprises navigate the transition from conservatorship to potential private ownership.

[1] Corrie Drebusch, AnnaMaria Andriotis, and Gina Heeb, Trump preparing IPO for Fannie Mae and Freddie Mac later this year, The Wall Street Journal, August 8, 2025, https://www.wsj.com/finance/regulation/trump-aiming-to-ipo-fannie-mae-and-freddie-mac-later-this-year-13b138cf.

[2] Fannie Mae Monthly Summary Highlights as of July 2025; Freddie Mac Monthly Volume Summaries July 2025, and Household Debt & Credit Report from the New York Fed as of June 2025.

[3] Wayne Passmore and Alexander H. von Hafften, GSE guarantees, financial stability, and home equity accumulation, Federal Reserve Bank of New York Economic Policy Review 24, No. 3, December 2018, https://www.newyorkfed.org/medialibrary/media/research/epr/2018/epr_2018_gse-guarantees_passmore.pdf.

[4] Darryl E. Getter, Fannie Mae and Freddie Mac in conservatorship: Frequently asked questions, CRS products (Library of Congress), July 22, 2020, https://www.congress.gov/crs-product/R44525.

[5] See “Senior preferred stock purchase agreement,” U.S. Federal Housing, FHFA.gov, https://www.fhfa.gov/conservatorship/senior-preferred-stock-purchase-agreements.

[6] Bureau of the Fiscal Service, Finance statement of the United States government for the fiscal years ended September 30 2024 and 2023, note 7. investments in government-sponsored enterprises, https://www.fiscal.treasury.gov/reports-statements/financial-report/balance-sheets.html.

[7] “Memorandum on federal housing finance reform”, The Whitehouse, March 27, 2019, https://trumpwhitehouse.archives.gov/presidential-actions/memorandum-federal-housing-finance-reform/.

[8] “Housing Reform Plan,” U.S. Department of the Treasury, September 2019, https://home.treasury.gov/system/files/136/Treasury-Housing-Finance-Reform-Plan.pdf.

[9] “Treasury Department and FHFA amend terms of Preferred Stock Purchase Agreements for Fannie Mae and Freddie,” U.S. Department of the Treasury, January 14, 2021, https://home.treasury.gov/news/press-releases/sm1236.

[10] “Enterprise regulatory capital framework final rule,” U.S. Federal Housing, December 17, 2020, https://www.fhfa.gov/regulation/federal-register/final-rule/enterprise-regulatory-capital-framework-final-rule

[11] Corrie Driebusch et al, Trump preparing IPO, August 8, 2025.

[12]“Trump says US to retain oversight, guarantees in Fannie Mae, Freddie Mac spinoff,” Reuters, May 27, 2025, https://www.reuters.com/business/finance/trump-says-us-retain-oversight-guarantees-fannie-mae-freddie-mac-spinoff-2025-05-27.

[13] Colin Robertson, What on earth is the Great American Mortgage Corporation? The Truth about Mortgage, August 11, 2025, https://www.thetruthaboutmortgage.com/what-on-earth-is-the-great-american-mortgage-corporation.

[14] Corrie Driebusch, Gina Heeb, and AnnaMaria Androtis, Big banks woo Trump for roles on blockbuster IPO, The Wall Street Journal, October 6, 2025, https://www.wsj.com/finance/banking/fannie-freddie-ipo-big-banks-6d8884aa.

[15] Michelle Celarier, Will Ackman finally cash in on his Fannie Mae and Freddie Mac “lottery ticket?” September 9, 2025, https://www.institutionalinvestor.com/article/will-ackman-finally-cash-his-fannie-mae-and-freddie-mac-lottery-ticket.

[16] Bureau of the Fiscal Service, note 7.

[17] Victor Whitman, Fannie Mae and Freddie Mac post strong earnings, but the reform outlook unclear, February 17, 2025, https://www.scotsmanguide.com/news/fannie-mae-and-freddie-mac-post-strong-earnings-but-the-reform-outlook-unclear/.

[18] Dan Primack, CoreWeave raised $1.5 billion in scaled-back IPO, Axios, March 27, 2025, https://www.axios.com/2025/03/28/coreweave-ipo-nvidia.

[19] See H.R, 1209 – End of GSE Conservatorship Preparation Act of 2025, https://www.congress.gov/bill/119th-congress/house-bill/1209.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.