February Mid-Month Market Update

Labor Market: Mixed Signals, Strong Payroll Surprise

Due to the second government shutdown, the monthly jobs report from the Bureau of Labor Statistics was delayed by several days. In the interim, a series of labor market releases pointed to potential softness in employment trends:

- 2/4/26 – ADP Employment Change (January): Private sector payrolls increased by just 22,000 jobs, well below expectations.

- 2/5/26 – Initial Weekly Jobless Claims: Claims rose to 231,000, an eight-week high.

- 2/5/26 – Revelio Non-Farm Employment: Reported a decline of 13,000 jobs in January, the weakest reading on record dating back to 2021.

- 2/5/26 – JOLTS Job Openings (December): Openings fell to 6.542 million, marking the third consecutive monthly decline and the lowest level since the pandemic.

- 2/5/26 – Challenger Job Cuts (January): Layoff announcements totaled 108,435, the highest level since 2009.

Collectively, these reports suggested mounting weakness in labor demand and raised concerns heading into the official payroll release.

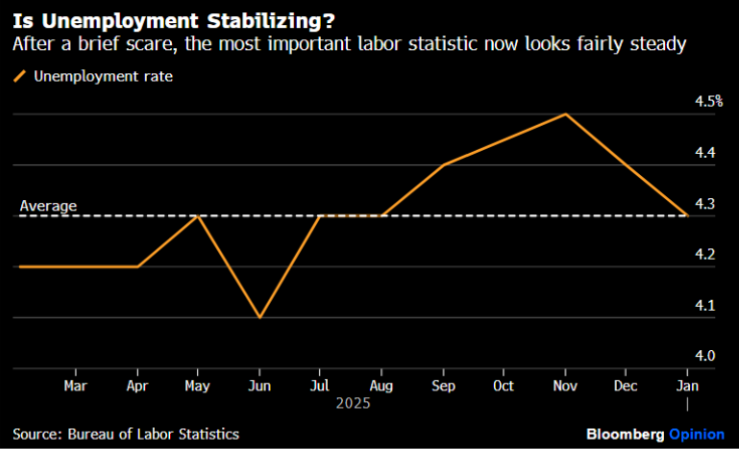

However, the January Non-Farm Payrolls (NFP) report, released on February 11th, delivered a meaningful surprise to the upside. Total payrolls increased by 130,000 — the strongest monthly gain in 13 months and well above the consensus estimate of 65,000.

The unemployment rate declined to 4.3%, or 4.283% unrounded, marking the lowest level since last July. Notably, the Labor Force Participation Rate increased during the month — a development that would typically place upward pressure on the unemployment rate. The fact that unemployment declined despite higher participation underscores the strength of hiring in January.

2025 was one of the weakest years for the labor market with just 181,000 jobs created, the lowest annual total during a non-recessionary period since 2003. However, the January NFP report suggests that 2026 has begun on firmer footing, even as several other labor market indicators remain mixed.

Inflation Update: Encouraging Trend, Sticky Components

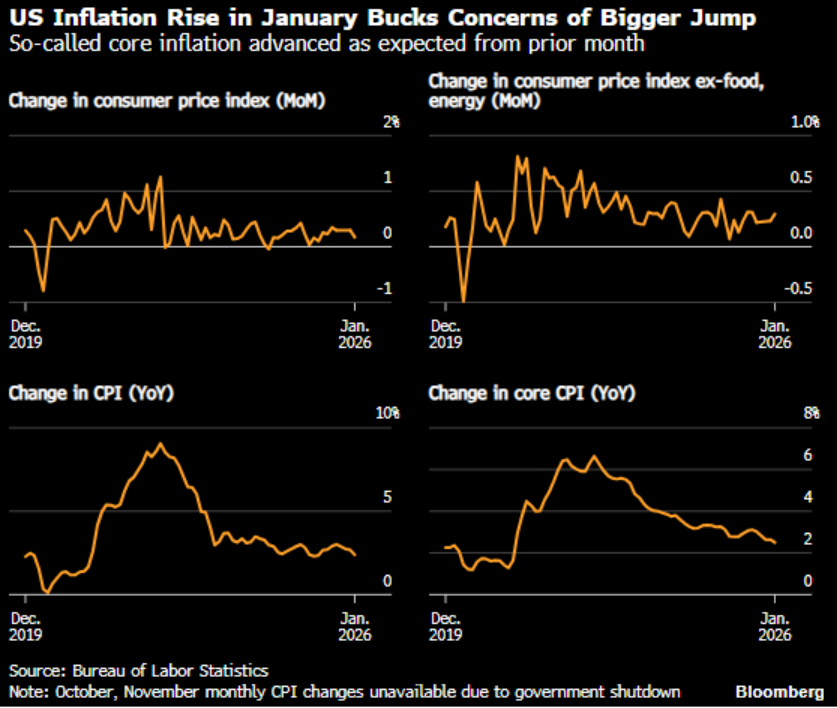

Historically, January inflation readings have tended to run firm and often come in above expectations, as companies use the start of the year to reset and raise prices for the months ahead. This year, however, January CPI surprised to the downside. Headline CPI rose just 0.2%, below expectations, while Core CPI increased 0.3%, in line with consensus. For comparison, January Core CPI rose 0.4% in both 2023 and 2025, and 0.6% in 2022 — reinforcing the market’s sensitivity to early-year inflation strength.

That said, the details were somewhat mixed. The Super-Core measure rose 0.6%, its largest monthly increase since January 2025, signaling ongoing stickiness in certain service categories. In contrast shelter, one of the primary drivers of elevated inflation in recent years, increased just 0.2%, its smallest monthly gain since September.

On a year-over-year basis, the data was more encouraging from the Federal Reserve’s perspective. Headline CPI declined to 2.4%, while Core CPI eased to 2.5%, the lowest annual readings since 2021. This improvement was aided by base effects, as the strong +0.5% reading from January 2025 rolled out of the 12-month calculation window.

Looking ahead, attention now turns to the Fed’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) Index. The December PCE report, scheduled for release on Friday, February 20th, is expected to show Core PCE rising to +2.9% year-over-year — still meaningfully above the Fed’s long-term target.

Market Performance: Volatility Drives Flight to Quality

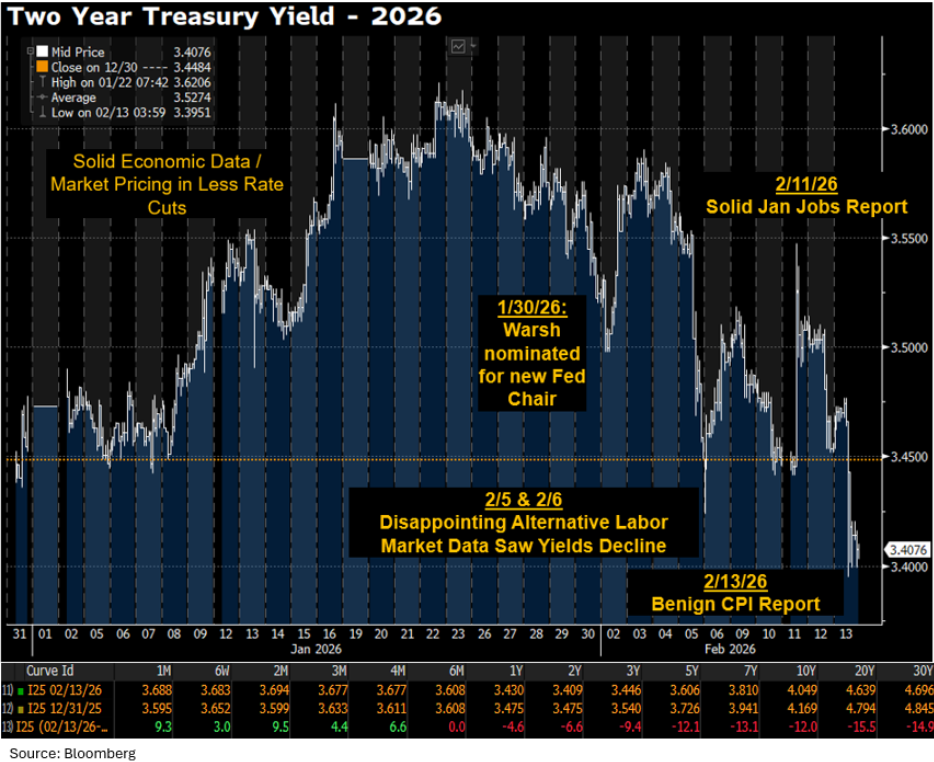

Treasury yields have been notably volatile this year, driven by a combination of mixed economic data, geopolitical developments, uncertainty surrounding the new Fed Chair nominee, and most recently, concerns about the implications of artificial intelligence for corporate America.

So far in February, market dynamics have reflected a clear flight-to-quality bid, with Treasury prices rallying as investors seek safety. On the equity side, more defensive sectors — particularly consumer staples and utilities — have outperformed other S&P 500 subsectors (see chart below), reinforcing the risk-off tone.

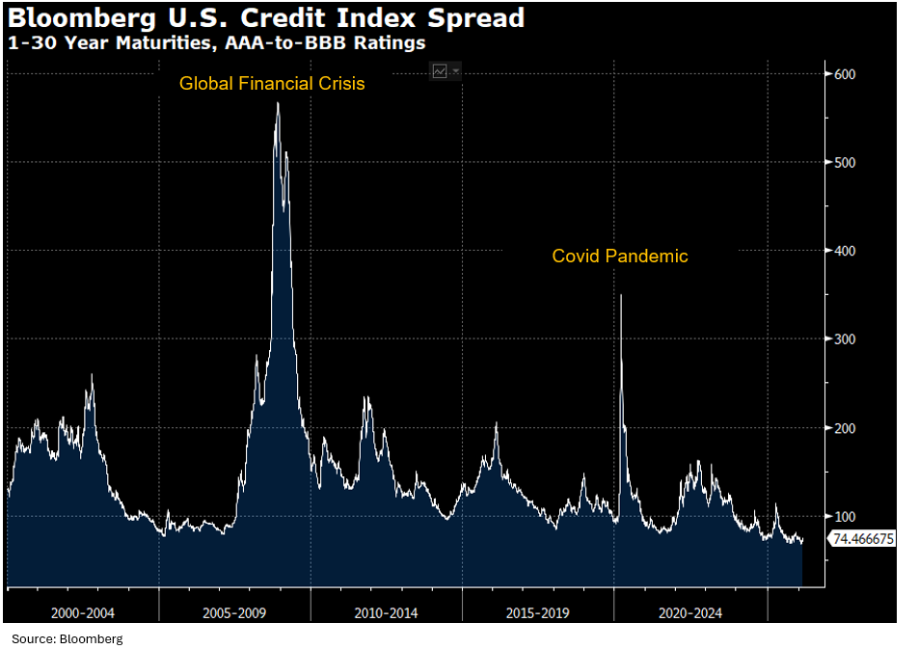

Despite the uptick in volatility and a backdrop of record corporate bond issuance, credit markets have remained resilient. Corporate bond spreads have held firm, tightening on a year-to-date basis and remaining near the narrowest levels observed over the past 26 years (see chart below).

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.