March Month-End Market Update

Q1 2026 Recap

Geopolitical tensions drove markets in Q1 2026, with the Iran conflict overshadowing much of the quarter. Early signs of escalation—highlighted by comments from Donald Trump in January—began pushing oil prices higher, though Treasury yields were initially driven by monetary policy expectations, reflecting markets anticipation for one to two rate cuts from the Federal Reserve.

Following the onset of military strikes on February 28, the narrative shifted sharply. Brent crude surged 94% to $118.35 per barrel by quarter-end—its largest quarterly gain since the Gulf War—fueling inflation concerns, pressuring equities, and driving Treasury yields higher. Other developments, including a ruling by the U.S. Supreme Court on global tariffs, were largely overshadowed by the Iran conflict in shaping first-quarter performance.

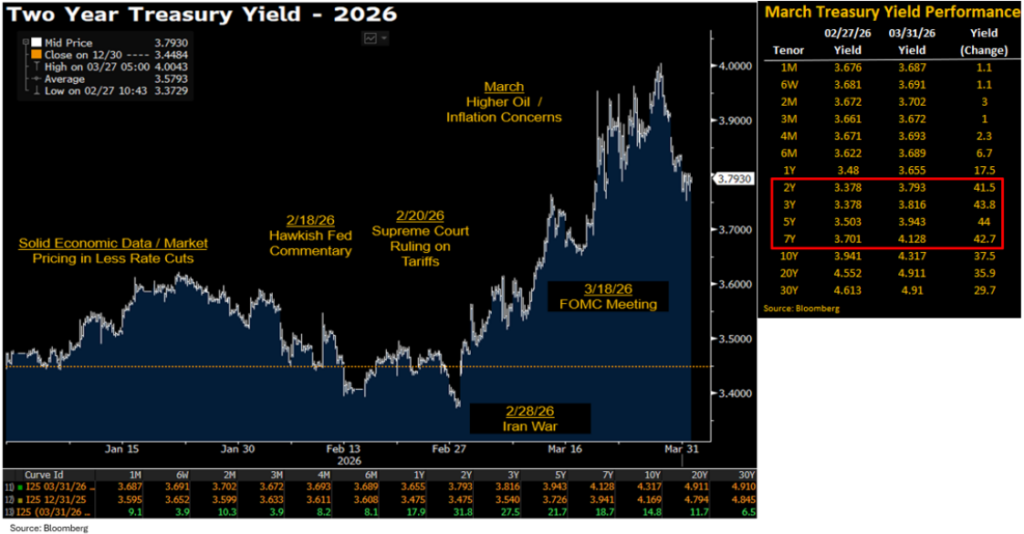

Treasury Yield Performance

U.S. Treasury performance in the first quarter was largely driven by the sharp repricing that occurred in March. Prior to the onset of the Iran conflict, yields across the curve—from 2 to 30 years—had been trending lower, reflecting expectations for upcoming rate cuts from the Federal Reserve. However, March marked a clear inflection point, with yields moving higher across the curve as the surge in oil prices reignited inflation concerns (see chart below).

Despite the broader market volatility, front-end credit has remained resilient. The Bloomberg 1–3 Year Credit Index is only 8 basis points wider year-to-date, indicating continued stability in high-quality, short-duration credit. Both the Nasdaq and Dow declined into correction territory, falling 10% from their recent highs, while the S&P 500 suffered its worst quarter in nearly 4 years.

More recently, Treasury yields have retreated from their March highs, as some market participants have begun to shift their focus from inflation risks toward concerns about slowing economic growth.

Fed Rate Cut Expectations Pushed Out

Throughout January and February, fed funds futures were pricing in one to two rate cuts in 2026 from the Federal Reserve. However, following the onset of the Iran conflict, expectations shifted materially, with markets pushing out the timing of rate cuts to 2027 and briefly assigning some probability to additional rate hikes.

More recently, commentary from Jerome Powell has helped temper concerns over the potential for higher overnight rates. Powell noted that longer-term inflation expectations remain “well anchored” and emphasized that policy is “in a good place” to remain patient. As a result, markets have reduced the probability of rate hikes, though they continue to price in no rate cuts in 2026 and only a gradual easing cycle beginning toward the end of 2027 (see chart below).

Stagflation concerns have driven a tug-of-war in market expectations, reflecting the tension between persistent inflation pressures and signs of slowing growth in the labor market and broader economy. For now, this dynamic is likely to keep the Fed on hold. While policymakers may look through the current oil shock if it proves temporary, a more prolonged energy disruption could shift the Fed’s tone in a dovish direction as higher energy costs weigh on growth.

Average gasoline prices rose above $4 per gallon for the first time since August 2022 and diesel climbed above $5 per gallon. A sustained period of elevated diesel prices in particular could ripple through supply chains, putting additional upward pressure on consumer prices. As a result, some economists expect headline inflation could approach 4% in the coming months.

Strait of Hormuz Reopening Remains a Key Catalyst

Since early March, shipping activity through the Strait of Hormuz has declined significantly, with only a limited number of cargo vessels transiting the straight (see chart below). As a critical artery for global energy supply, the trajectory of oil prices—and financial markets —will be heavily dependent on when normal shipping flows resume.

Heading into late March, there were signs of cautious optimism that the conflict could move toward a resolution. Commentary from Donald Trump signaling a desire to end the war, alongside remarks from Masoud Pezeshkian indicating Iran’s willingness to de-escalate under certain conditions, raised expectations for potential negotiations. While a near-term agreement remains uncertain, these developments suggested a possible path toward stabilization.

However, more recent messaging has introduced renewed uncertainty. In a mid-week address, President Trump delivered mixed signals—stating that objectives were “very close” to completion, while also indicating the U.S. could intensify military action in the coming weeks. Rather than providing a clear off-ramp, the comments pointed to the potential for further escalation, prompting a renewed rise in both oil prices and Treasury yields.

Ultimately, the Iran conflict presents a dual risk to markets—upside pressure on inflation and downside risks to growth. The duration of the disruption, particularly with respect to energy flows, will be a key determinant of the magnitude and persistence of its impact on the global economy.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.