April Mid-Month Market Update

March Labor Market Data Rebounds

Labor market data showed signs of improvement in early April, following February’s weaker-than-expected report:

- ADP private payrolls came in above expectations with 62,000 jobs added in March.

- Weekly jobless claims declined to the second-lowest level of the year, reinforcing the ongoing “low hire, low fire” dynamic.

- The March employment report also surprised to the upside, with nonfarm payrolls increasing by 178,000, rebounding from February’s revised decline of 133,000.

While the unemployment rate edged lower to 4.3% (4.256% unrounded), the improvement was driven in part by a decline in the labor force participation rate, which fell to its lowest level since 2021 as nearly 400,000 individuals exited the labor force.

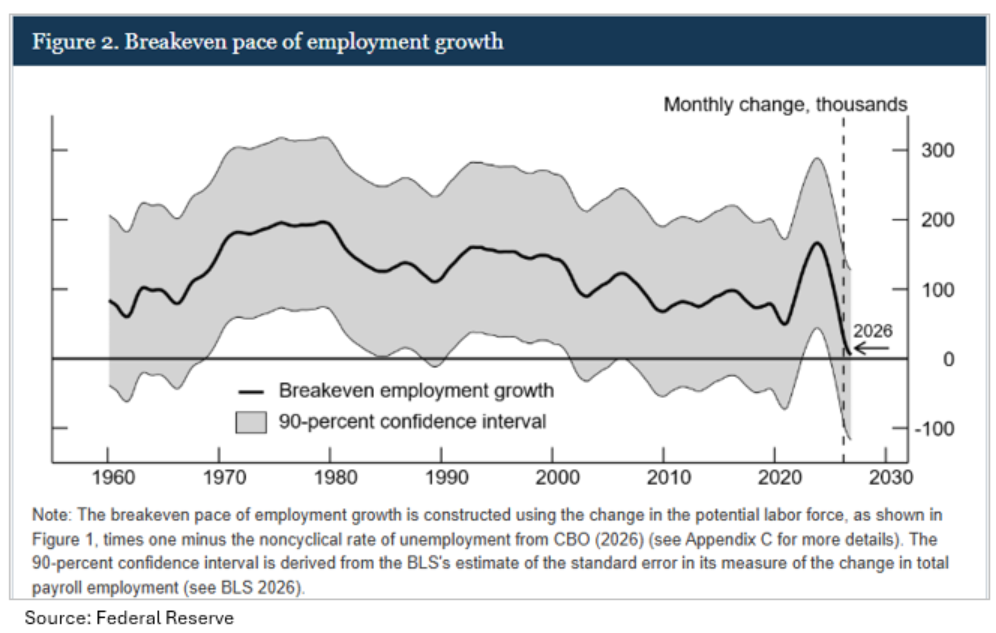

The Federal Reserve also highlighted a notable shift in the labor market backdrop, pointing to a decline in the “breakeven” pace of employment growth—the level of job creation needed to keep the unemployment rate stable. This threshold has fallen to near zero, with fewer than 10,000 jobs per month needed in 2026, compared to roughly 155,000 in 2023–2024, when stronger labor force growth—driven in part by elevated immigration—required a much higher pace of hiring (see chart below).

Inflation Pressures from the Iran Conflict

March economic data underscored the inflationary impulse stemming from the Iran conflict, particularly through higher energy prices and input costs:

- The ISM Manufacturing Prices Paid rose to its highest level since June 2022.

- The ISM Services Prices Paid surged to its highest level since October 2022, with the 7.7-point increase marking the largest monthly gain since August 2012.

- The Consumer Price Index (CPI) posted its largest monthly increase since January 2022, rising 0.9%. The move was driven by a 21.2% surge in gasoline prices—the largest monthly increase on record dating back to 1967—which pushed the year-over-year rate up from 2.4% to 3.3%.

Encouragingly, core inflation showed signs of moderation, with Core CPI rising just 0.2% in March. Food prices were flat on the month, while declines in used car and medical care prices helped offset broader inflation pressures.

As of 4/15/26, oil prices—including WTI crude and Brent crude—have retreated from their peaks amid growing optimism around a potential de-escalation (see chart below). Reports of an “in principle” agreement between the U.S. and Iran to pursue further diplomacy, along with mediation efforts ahead of the April 7 truce deadline, have helped ease near-term supply concerns and stabilize energy markets.

Risk Assets Rally While Rate Cuts Remain Distant

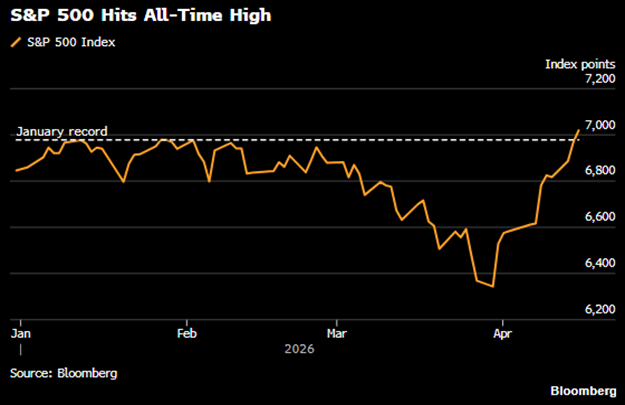

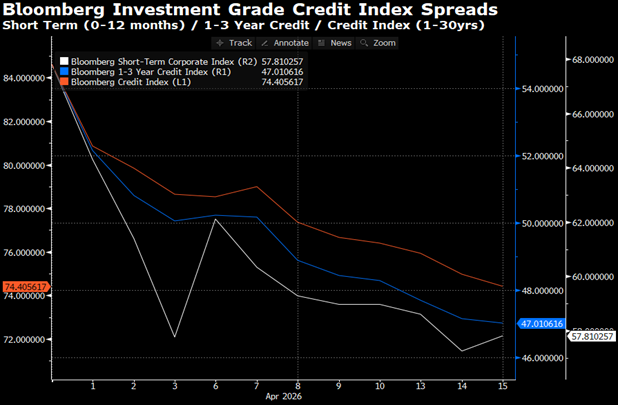

Equity markets rallied in April, with the S&P 500 advancing nearly every day this month, rising +10.7% over the last 11 trading days and closing above 7,000 for the first time on April 15th. Credit markets have also strengthened, with both investment grade and high yield spreads tightening amid growing optimism around a Middle East ceasefire, stable economic data, and resilient corporate earnings.

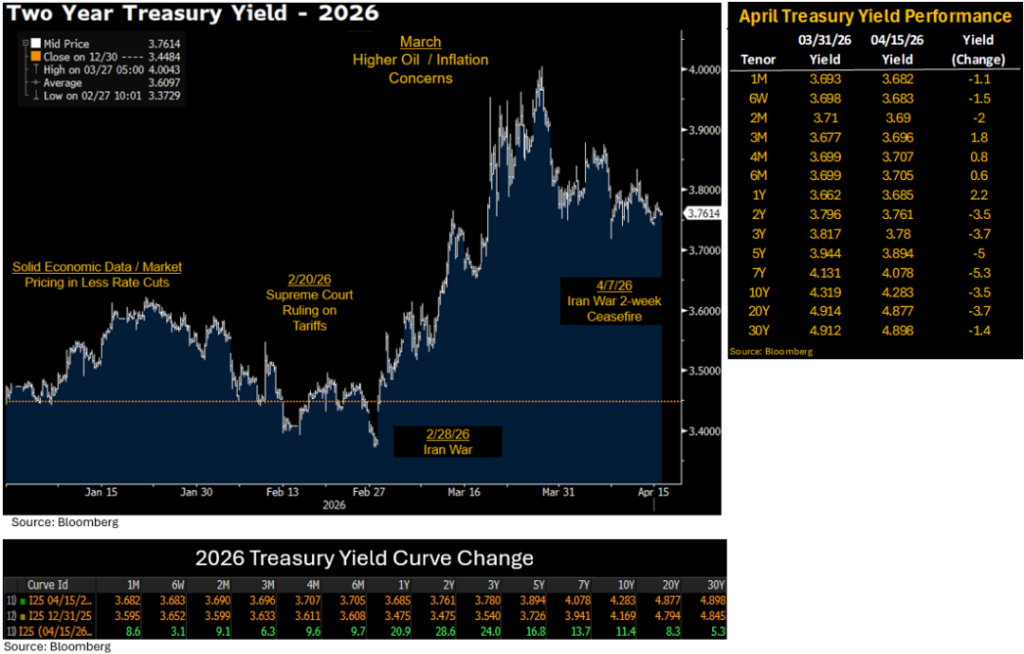

Treasury yields have been mixed but largely unchanged this month. The 2-year Treasury yield—typically the most sensitive to shifts in monetary policy expectations—declined modestly by approximately 3 basis points through April 15th but remains 38 basis points higher than the day before the Iran war began.

Despite the constructive market backdrop, Federal Reserve communication has kept a hawkish tilt. Cleveland Fed President Beth Hammack noted that her baseline expectation is for policy to remain on hold for an extended period, while acknowledging “two-sided risk” to rates. This tone was echoed in the March Federal Open Market Committee minutes, where participants said “the risk of inflation remaining elevated for longer than expected amid a persistent increase in oil prices, which could call for rate increases to help bring inflation down to the Committee’s 2 percent objective and keep longer-term inflation expectations firmly anchored.”

Reflecting this backdrop, fed funds futures continue to price in no rate cuts in 2026, with the first easing not expected until mid-2027.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.