April Month-End Market Update

Fed on Hold, But Tilt Shifts Hawkish as Dissents Rise

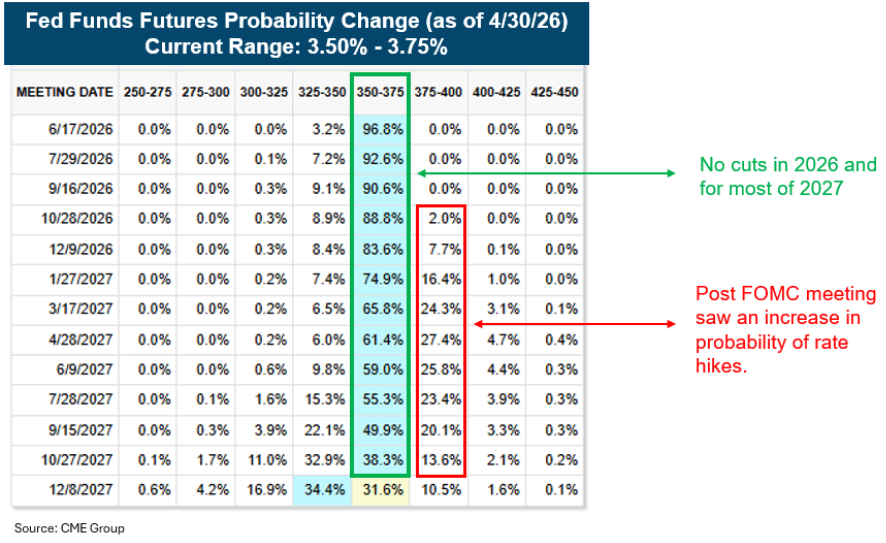

At its April 29th meeting, the Federal Open Market Committee held the federal funds target range steady at 3.50%–3.75%. Notably, the decision included four dissents, the most since 1992. Governor Stephen Miran dissented in favor of a 25 basis point rate cut, while Cleveland Fed President Beth Hammack, Minneapolis Fed President Neel Kashkari, and Dallas Fed President Lorie Logan dissented in opposition to the inclusion of an easing bias in the policy statement, but supported holding rates at their current level.

Following the meeting, each dissenting regional president provided additional context:

- Cleveland President Hammack: Emphasized heightened uncertainty around the economic outlook, arguing that this environment does not justify maintaining an easing bias. She noted that language referencing “additional adjustments” was originally intended to signal a pause rather than the end of an easing cycle, and views that guidance as no longer appropriate given current conditions.

- Minneapolis President Kashkari: Echoed concerns about retaining easing bias language and outlined potential risk scenarios, including a prolonged closure of the Strait of Hormuz. In such a scenario, he warned that both inflation and unemployment could rise, potentially requiring a forceful policy response, including a series of rate hikes despite potential labor market weakness.

- Dallas President Logan: Highlighted the high degree of uncertainty in the outlook, noting that inflation could remain elevated or moderate, while labor market conditions could either strengthen or weaken. As a result, she emphasized that the next policy move could plausibly be either a rate hike or a cut.

At his press conference, Jerome Powell described a “vigorous” debate around the guidance language in the statement, noting that a growing number of Committee members could support shifting to a more neutral stance—where a rate cut is viewed as just as likely as a hike. While Powell emphasized that “nobody’s calling for a hike right now,” he reiterated that “if we need to hike, we will certainly signal that and we will certainly do it.”

Taken together, the tone reflects a modest hawkish shift within the Committee, contributing to higher Treasury yields across the curve and prompting the fed funds futures market to begin pricing in the possibility of rate hikes (see chart below).

Staying on as Governor

Although this marked his final meeting as Chair of the Federal Open Market Committee, Jerome Powell confirmed he will remain on the Federal Reserve Board after his term as Chair ends on May 15th. While encouraged by recent developments involving the U.S. Department of Justice, Powell stated he does not intend to step down “until this investigation is well and truly over, with transparency and finality.” He indicated he will remain a governor for an undetermined period and maintain a lower public profile, citing concerns that increasing legal and political pressures could undermine the Fed’s independence in conducting monetary policy.

Warsh Moves Closer to Confirmation

Fed Chair nominee Kevin Warsh has been approved by the U.S. Senate Banking Committee, with the next step being a full Senate confirmation vote. Given the current Republican majority, confirmation is widely expected, with a vote anticipated in the near term.

Bottom Line

The Fed appears set to remain on hold for the foreseeable future, as mixed economic data and ongoing geopolitical risks shift the Committee away from an easing bias toward a more balanced, two-sided policy stance. As incoming Chair, Warsh is likely to inherit a divided Fed that is hesitant to cut rates, while also facing external pressure from the Trump Administration for easing despite persistent inflation concerns.

Q1 GDP Supported by AI Investment and Resilient Consumer

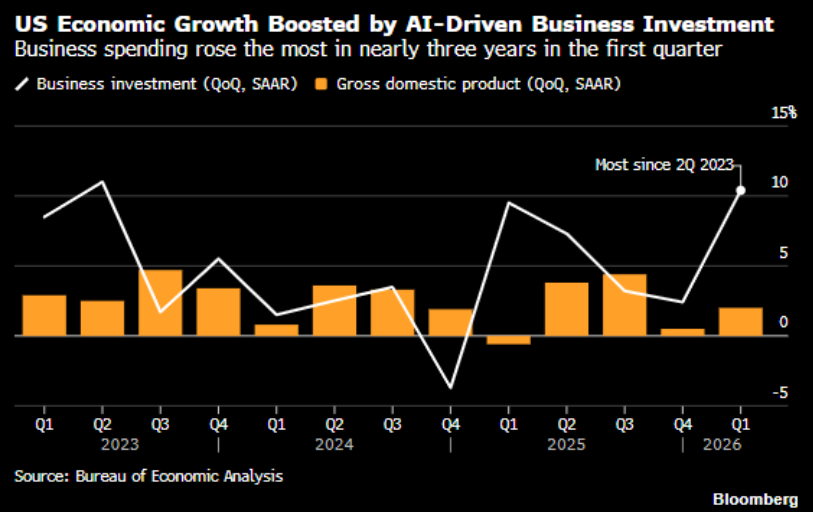

U.S. economic growth remained solid in the first quarter, supported by a surge in AI-driven investment and continued resilience in consumer spending. Real GDP increased by 2.0%, coming in above the Federal Reserve Bank of Atlanta’s GDPNow estimate of 1.2%, though modestly below market expectations of 2.3%.

Consumer spending rose 1.6%, exceeding expectations, driven by strength in financial services and healthcare. Alongside better-than-expected retail sales earlier in the month, the data points to a consumer that remains resilient despite higher energy prices.

The standout component of the report was business investment, which surged 10.4%—the fastest pace in nearly three years—led by rapid growth in AI-related spending. Outlays on information processing equipment jumped 43%, while software investment surged 184%, underscoring the accelerating pace of digital and AI adoption.

The slightly softer headline GDP figure was largely attributable to a drag from imports, which subtracted approximately 1 percentage point off growth. This reflects the fact that much of the AI-related equipment is sourced internationally. Recent earnings reports from major cloud and technology firms reinforce this trend, and with capex plans continuing to rise, AI investment is likely to remain a key driver of U.S. economic growth.

April 2026 Recap: Risk Assets Rally Amid Uncertainty

The Iran conflict and resulting volatility in oil prices dominated market headlines in April. Following the April 7th ceasefire announcement, markets shifted into a risk-on tone that persisted through month-end, even as negotiations failed to produce a lasting agreement. While rising oil prices kept inflation concerns elevated—and central bank rhetoric remained broadly hawkish—risk assets proved resilient and broadly outperformed.

- Equities: The S&P 500 gained 10.5%, marking its strongest monthly performance since November 2020, while the Nasdaq Composite surged 15%, its best month since April 2020.

- Treasuries: Yield movements were mixed. Front-end yields (out to 6 months) declined, while yields from 1 year to 30 years moved higher. The 2-year and 3-year led the move, rising approximately 7 basis points to 3.87% and 3.89%, respectively.

- Credit: Credit markets strengthened, with both investment grade and high yield spreads tightening. Demand for new issuance remained robust, with approximately $285 billion priced in the investment grade market, making it the second-largest issuance month on record.

- Oil: Oil prices were highly volatile. Brent crude entered the month at $118.35, fell to a low of $90.38 on April 17th amid optimism around a potential resolution, and ultimately closed at $114.01 as renewed concerns over a prolonged conflict emerged, including risks tied to a U.S. blockade.

- Dollar: The U.S. Dollar Index declined 1.9%, its largest monthly drop since August, underperforming all G10 currencies.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.