August 2025 Month-End Market Update

Powell Cracks the Door Open to a September Cut

At the Jackson Hole Symposium on August 22nd, Fed Chair Jerome Powell signaled that the first rate cut of 2025 could be on the table at the September FOMC meeting, noting that “the shifting balance of risks may warrant adjusting our policy stance.” His more dovish tone followed the weaker-than-expected August employment report, with Powell acknowledging that “downside risks to employment are rising.”

Still, the Fed remains divided. Most expect policymakers to favor a cautious 25 bp cut rather than a more aggressive 50 bp move. That same morning, Boston Fed President Susan Collins warned that “it’s not a done deal in terms of what we do at the next meeting,” while Chicago Fed President Austan Goolsbee highlighted the latest spike in services inflation as “a dangerous data point.”

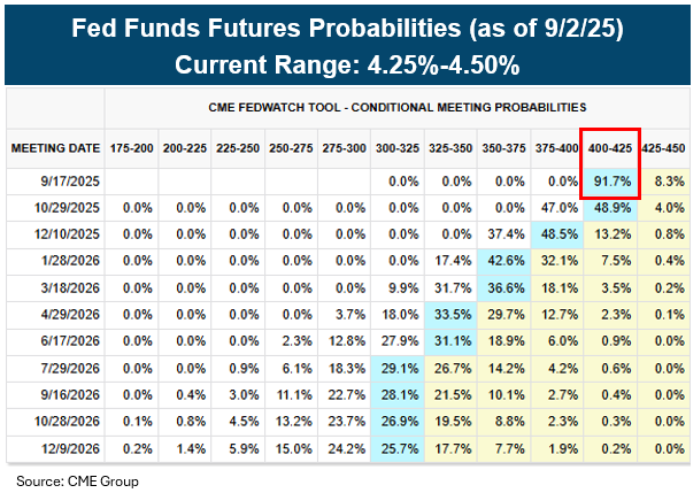

Despite the debate inside the Fed, markets appear more certain: Fed fund futures are pricing in better than a 90% probability of a 25 bp cut at the September 17th meeting.

Rising Inflation Pressures Resurface

Recent August data and corporate commentary point to renewed upside pressure on inflation:

- PMI and ISM: Prices paid components moved higher, with ISM Prices Paid hitting its highest level since October 2022 (see chart below).

- Regional Fed Data: The Philadelphia Fed Business Outlook reported prices paid at a 3-year high.

- Consumer Expectations: The University of Michigan survey showed consumers expect prices to rise 4.8% over the next year.

- Core PCE: The Fed’s preferred inflation gauge rose +0.27% in July, the strongest monthly gain since February.

- Market Pricing: 2-year inflation swaps climbed to 3.08%, the highest since late 2022 when CPI was 6.5%.

- Corporate Insights: Walmart’s CEO noted that replenishing inventory at post-tariff prices has led to “continued cost increases each week,” with pressure expected to persist through Q3 and Q4.

Bond Market Rallies as Yields Extend August Decline

Treasury yields continued to fall in August, led by the 2-year, which dropped 34 bps to 3.62%—its largest monthly decline since August 2024. The move followed Chair Powell’s August 22nd Jackson Hole speech, where he signaled openness to a policy shift. In credit, high yield bonds strengthened, with yields falling and spreads tightening to six-month lows. Equities also rallied: the S&P 500 and Nasdaq extended record highs, while the Dow Jones Industrial Average posted its first record close of the year. Meanwhile, gold surged to a record $3,448/oz as inflation concerns gained traction.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.