July 2025 Month-End Market Update

Powell Maintains a Hawkish Stance Amid FOMC Dissent

Last week the FOMC, as expected, left the federal funds target range unchanged at 4.25%–4.50% for the fifth consecutive meeting. Notably, two Federal Reserve governors—Christopher Waller and Michelle Bowman—dissented, each favoring a 25 basis point cut. While regional Federal Reserve Bank Presidents have dissented more frequently, this marked the first dual dissent by members of the Board of Governors at an FOMC meeting since 1993.

The official statement maintained that labor market conditions remain solid and inflation remains elevated. However, it included a slight economic downgrade, noting that “economic activity moderated in the first half of the year”—a softer tone than June’s assessment that the economy was growing at a “solid pace.”

Fed Chair Powell struck a hawkish tone during his press conference. Key highlights included:

- Powell reiterated that the economy remains in a solid position, while acknowledging the uncertain impact of evolving government policies.

- He noted that “higher tariffs have begun to show through more clearly to prices of some goods.”

- When asked about tariff-driven inflation, he responded, “You could argue we are a bit looking through goods inflation by not raising rates,” suggesting that rate hikes remain a possibility if tariffs prove inflationary.

- Powell emphasized that the full impact of tariffs is still unclear, stating, “we think we have a long way to go to really understand exactly how it will be,” suggesting the timing of rate cuts could be pushed out.

- On the labor market, Powell pushed back against concerns of weakening, pointing to stable trends in quits, job openings, and the unemployment rate. He added that the Fed is applying less emphasis on the headline job numbers because those figures have been declining alongside a decline in labor supply.

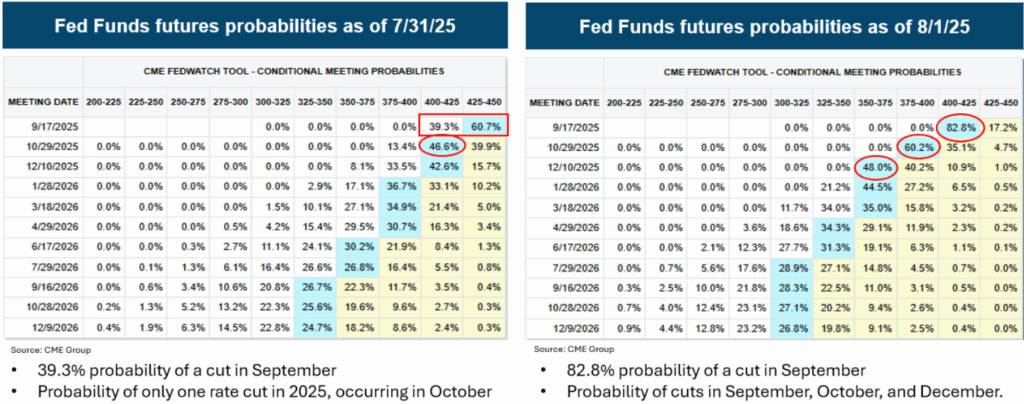

Markets reacted with a rise in Treasury yields across the curve, led by the 2-year, which climbed over 7 basis points to 3.941%. Following the FOMC meeting, fed funds futures markets significantly lowered the odds of rate cuts in 2025. Prior to the meeting, markets had priced in two cuts this year, with a greater than 70% chance of the first occurring in September. After the meeting, those odds dropped below 40%, with just one total cut priced in for 2025. However, these expectations shifted again following the July employment report released on August 1st (see below).

Economic Data Sends Mixed Signals

Data released in July was mixed, highlighting continued strength in consumer activity but growing signs of weakness in the labor market. The Fed’s dual mandate—maximum employment and price stability—appears to be increasingly at odds, as inflation remains stubbornly above the 2% target and thus making the path for monetary policy more uncertain. Key highlights from the recent data include:

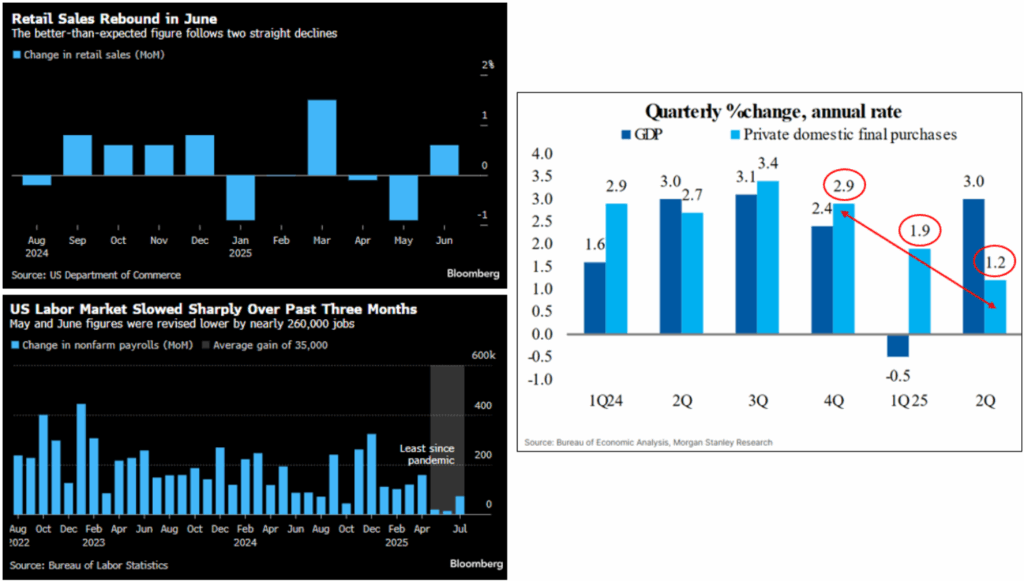

- Retail Sales (June): Consumer spending came in stronger than expected, with headline retail sales rising +0.6% vs. +0.1% forecast. The Control Group—a key input to GDP—also beat expectations, increasing +0.5% vs. +0.3%. Gains were broad-based, with 10 of 13 categories posting increases, offering some relief to markets following two consecutive monthly declines (see chart below).

- Q2 GDP: The economy rebounded in the second quarter, with initial GDP growth at +3.0%, ahead of the +2.6% consensus. The improvement was largely driven by a reversal in imports. Personal consumption also recovered, rising +1.4%, up from +0.5% in Q1. However, private domestic final purchases—which exclude government spending and net exports—suggest underlying growth is slowing. This metric rose +1.2% in Q2, down from +1.9% in Q1 and +2.9% in Q4 2024 (see chart below).

- July Employment Report: The labor market showed broad-based weakness. Nonfarm payrolls increased by just +73,000, well below expectations. Even more concerning were 258,000 in cumulative downward revisions to May and June. June was revised from +147,000 to +14,000, and May from +144,000 to +19,000—marking the lowest monthly gains since the onset of the COVID-19 pandemic. The three-month average fell to +35,000, the weakest since June 2020. Meanwhile, the unemployment rate rose to 4.2%, narrowly missing a new cycle high of 4.3% on an unrounded basis.

Fed Funds Probabilities Whipsawed

For most of the year, the Fed funds futures market has been pricing in 50 to 100 basis points of rate cuts in 2025. However, expectations have been highly volatile in response to shifting data and Fed commentary. Below is a summary of recent movements in 2025 rate cut expectations:

- Late June: Markets priced in 75 basis points of rate cuts after Fed Governors Waller and Bowman signaled support for a cut at the July FOMC meeting.

- Early July: Expectations fell to 50 basis points following a stronger-than-expected employment report.

- Post-FOMC (July 30): After a hawkish-leaning press conference by Chair Powell, the market scaled back to just 25 basis points of expected cuts.

- After August 1 Employment Report: Following a weaker-than-expected jobs report, expectations jumped back to 75 basis points of cuts, with the probability of a September rate cut surging to over 80%, up from just 39% prior to the report.

Treasury yields were also whipsawed over the past week—rising from a hawkish Powell at the FOMC meeting, only to reverse sharply as the two-year Treasury yield declined 27 basis points following the disappointing August 1st employment report.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.