March 2025 Month-End Market Update

Q1 2025: The Trump Trade Unwound on Tariff Concerns

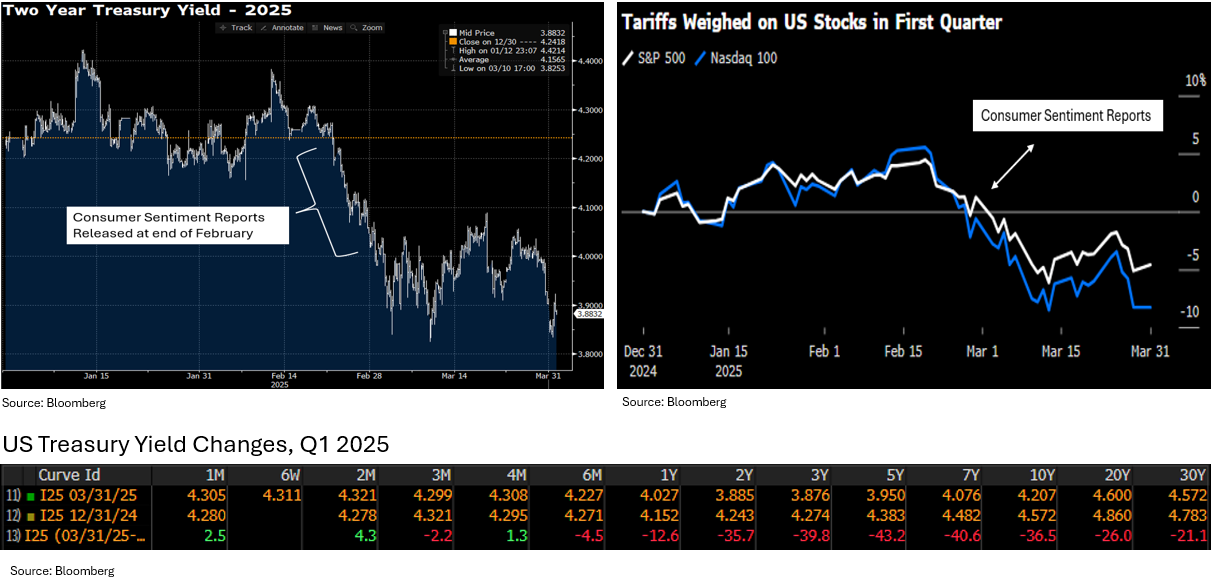

First quarter market activity was driven by tariff headlines along with increased fears of inflation and slowing growth. These concerns fueled a significant drop in consumer sentiment, which led Treasury yields to rally and U.S. equities to decline (see charts below). The first three months of the year also included significant disruption in the AI sector with the release of DeepSeek and an outperformance in European equities due to a shift towards higher defense spending.

- Treasury yields in the 2-to 30-year part of the curve declined by 20 to 40 basis points while front-end yields were little changed as they are highly correlated to the current fed funds rate.

- All 3 major US equity indexes declined, led by the Nasdaq and S&P 500, falling 10.42% and 4.59%, respectively. It was the worst quarter for both indexes since 2022.

- Although equity indexes fell, there was a shift to defensive sectors including Health Care (+6.08%), Consumer Staples (+4.58%) and Utilities (+4.12%).

- Investment grade credits returned +1% to -2% across the maturity curve. Within the front-end, the Bloomberg Short Term Corporate Index spread tightened 15 basis points while the Bloomberg 1-3 Year Corporate Index held in well, widening only 4 basis points during the quarter.

- Inflation concerns helped drive gold to become the best performing asset class, rising 19%, the highest quarterly increase since 1986.

Source: Bloomberg

Fed Speakers Refrain From Using the “T” Word

At the March FOMC meeting, Fed Chair Powell brought back a word that still haunts him after its use to describe the impact on prices from the Covid pandemic: “transitory”. Powell acknowledged that tariffs may delay “further progress” on inflation but said that the base case was that tariffs’ impact on inflation would be “transitory.” Many market participants commented that they gasped when they heard Powell use the “T” word again. In addition, several Fed members have come out against using the term “transitory” indicating there may be disagreement within the Fed over the inflation outlook:

- Atlanta Fed President Raphael Bostic: He was asked about his take on using the word “transitory” regarding tariff inflation and he said: “I’m not going to say that word. Nope.”

- St. Louis Fed President Alberto Musalem: “I would be wary of assuming that the impact of tariff increases on inflation will be entirely temporary.”

- Boston Fed President Susan Collins: “It looks inevitable that tariffs are going to increase inflation in the near term”, adding that “depending on how things unfold, it may be more persistent and a larger increase.”

Sticky Inflation

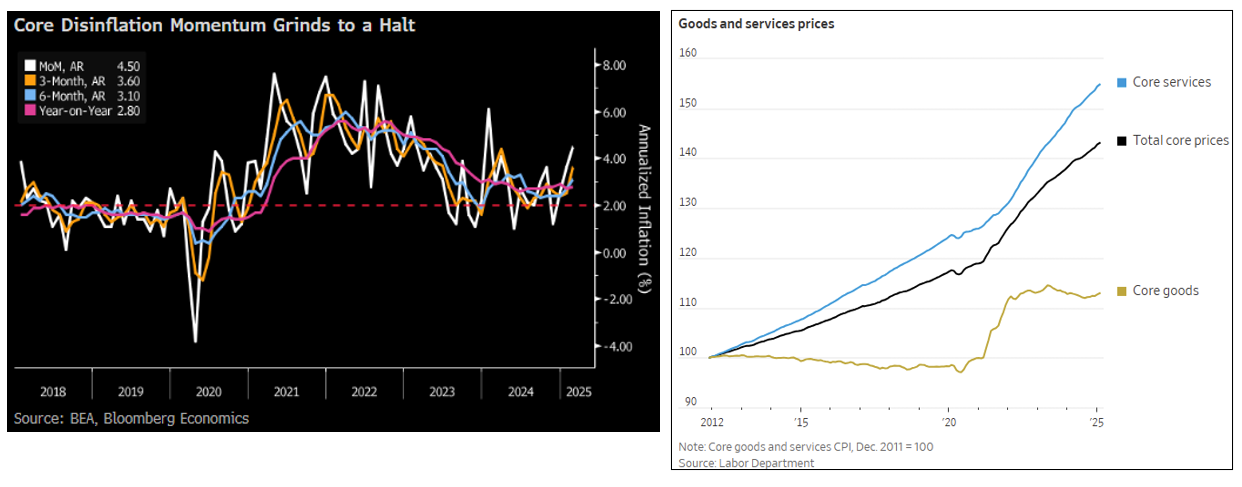

The Fed’s preferred inflation gauge, the Core PCE Deflator, came in higher than expected at +0.4% (0.365% unrounded) for February, which was the largest monthly gain since the beginning of 2024. This brought the 3-month annualized rate up to +3.6%, the 6-month pace to +3.1% and the one-month pace to +4.5%. The year-over-year reading rose back to +2.8% (see chart below).

Core goods prices (ex-food & energy) have been rising, and highlight an important inflation dilemma for the Fed. From 2011 to 2019, core goods prices declined while core services rose +2.7% year (see chart below). Following a significant spike during the pandemic, prices for goods have recently been rising by an average of +0.1% per month. This means that core goods are no longer providing a deflationary offset to high and sticky services inflation.

Source: Bloomberg

This information was prepared by Capital Advisors Group, Inc. from outside sources which we believe to be reliable. However, we make no representations as to its accuracy or completeness. The economic statistics presented in this report are subject to revision by the agencies that issue them.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.